2023.10.09 Weekly Notes

Whilst I maintain my tactically bullish risk stance, this week I consider the possibility of where we could go from here particularly on the growing sense that yields may be plateauing as growth-concerns takes centre-stage with stagflation risks in the rear-view:

- inflation pressures waning — reacceleration fears has likely abated after the sure in Oil prices got completely unwound last week with WTI closing the week just below $83/bbl after reaching within a cent of the 95 handle a week prior. Core inflation and wage growth trends are continuing to ease gradually also, and tight consumer and commercial credit conditions is likely to keep supporting that trend.

- growth slowing — major economies are stagnating and increasingly expected to tip into recession next year, and this is likely to put a strain on further advances and in yields with bond yields already at high levels. For the US, the growth picture is looking much more solid as evidenced by last week’s PMIs but there are other indications that risks are now to the downside for the US consumer — e.g. very high cost of mortgage and credit card debt, the latter of which is piling up against dwindling savings, student load repayments starting to tighten up the purse, commercial credit contraction, loan delinquencies and company bankruptcies rising.

Since the surge in yields was a major source of market volatility; it stands to reason, and perhaps ironically that growth-concerns will help to abate that recent volatility. Barring any sudden price shocks, current yield levels becomes more attractive as recession risks increases and should therefore improve investor appetite for bonds which would see yields plateau, and gradually recede.

Last week we saw 10 and 30year real yields climb above their breakeven inflation rates, and this causes me to believe that policy rates have reached where they need to be, Fed has got their wish, and these moves therefore helps the Fed lean towards being on pause (and done).

What’s interesting is that the last time we saw positive real rates was during the pause in 2006–07 — SPX went on to put in ~15% rally in the 6months after the last hike on 29Jun’06, continued to rally up until mid’07 when the Subprime crisis became apparent, and at which point bonds started to perform again. There is a lot fed speeches on deck this week and I will be particularly focused on whether we start to see hints of the Fed dialling down on their hawkishness as a result of recent rates market moves as we saw with Daly last week:

Should we hear more changes in tone, pricing for hikes should get incrementally priced out and cuts pulled forward, all of which would help to stabilise market volatility.

This week we have inflation data and treasury auctions totaling 100billion in supply. I would agree with Stephen there is already a lot in the price at these yield levels and if we get through these event without getting stretched further, I’d say there’s a very good chance we may have seen the peak in bear steepening.

To take the above a few steps further…

We have been seeing a broad normalisation in the labour market and economic activity (e.g. wages and inflation cooling, services easing while manufacturing rebounds), and assuming that gradual trajectory continues in the months ahead — ‘a harmonious balance of inflation easing and growth slowing but not too rapidly’, add to that the possibility of a decent earnings season on the robust economic data we’ve seen in Q3 as noted in prior weeks, then I think we have strong chances of a major rally into year-end as rates and equity vol suppresses and upward momentum gains traction.

So… SPX to retest or even push to new ATH’s from here?

NEWSFLOW

MARKETS

- Wall Street Stock Traders Refuse to Break in Week of Treasury Turmoil (BBG). Stocks Open Lower After Strong Jobs Report (Barrons). Stocks Rally as Market Digests Strong Jobs Data (Barrons). Inside Today’s Jobs Report: 885,000 Full-Time Jobs Lost, 1.127 Million Part-Time Jobs Added, Record Multiple Jobholders (ZH). U.S. stocks stage a surprising rally on Friday. But can the party last? (MW). The stock market is building up to a major ‘buy’ signal (MW). Buy the Dip in Global Stocks as Rates Peak, Citi Strategists Say — Expects 15% upside in MSCI AC World Local index by mid-2024, Prefers cyclicals on mild economic slowdown, cooling inflation (BBG). Bonds to ‘Rally Big’ in 2024 Amid Recession, BofA’s Hartnett Says — Expects bonds to be best-performing asset in 2024 first half, Says recession or credit event will trigger policy easing (BBG).

- Treasury rout bolsters view that Fed will call time on rate rises (FT). El-Erian: The US may no longer avoid a recession (FT). Fading Optimism on Rates Signals Trouble Ahead for $425 Billion Debt Wall — Strong jobs report reinforces likelihood of higher for longer, No new junk bonds were launched in US as risk appetite falls (BBG). A Worrying Crack Just Appeared in the Credit Market — The correlation between rates and credit spreads is now positive (BBG). Bank of America Forecasts $400 Billion of Muni Sales in 2024 (BBG). Rate Cliff Awaits Global Economy After Higher-for-Longer Plateau — Quarterly outlook on what to expect from monetary policy, Fed and ECB seen cutting rates by middle of next year (BBG). ‘Last mile’ of disinflation the hardest, warns ECB deputy head (FT).

- Distressed Debt Anxiety Is Spreading Across Emerging Markets — 21 emerging-market countries trade at or near distressed, Restructuring talks see more snags as capital access dries up (BBG). Emerging economies face China and rate pressures as IMF, World Bank meet — Emerging markets at mercy of Federal Reserve, Impact of China’s slowdown uncertain, Debt in the spotlight at IMF meetings, Argentina, Pakistan, Kenya finances in focus (RTS).

- Yen Surges From Weakest Level in a Year Amid Intervention Talk (BBG). Euro Parity Is Back on the Market’s Radar as US Yields Surge — Common currency is down about 6% since peaking in July, Options show chance of euro trading at par with dollar rising (BBG).

- As Israel-Hamas War Rages, Oil Traders Focus on Iran — Traders don’t expect huge price reaction; escalation is key, Shipping routes are also in focus as well as the US response (BBG). Saudis to Stick With 1 Million-Barrel Oil Supply Cut For Now — Output curbs total more than 1 million barrels per day, Monitoring committee doesn’t recommend any policy changes (BBG). Hedge Funds Began Dumping Bullish Oil Bets Ahead of Price Rout — Net longs still held near a two-year high when market crashed, Money manager slashed bullish gasoline bets before US data (BBG). Exxon Sees $2.1 Billion Earnings Lift From Oil Prices, Refining — Gains partially offset by declining chemical margins, Guidance sets tone for oil majors’ third-quarter results (BBG). ExxonMobil in talks to buy US shale behemoth Pioneer — Potential deal would be oil supermajor’s biggest for almost a quarter of a century (FT). Australia LNG Workers Set to Resume Strikes as Prices Rise — Workers at Chevron plants voted to continue walkouts, Strike threats roiled global natural gas markets last quarter (BBG). Hedge Funds Most Bearish on Grains Since Early Pandemic Months (BBG).

AMERICAS

- US job growth sizzles in September; wage inflation cooling — Nonfarm payrolls increase 336,000 in September, Unemployment rate unchanged at 3.8%, Average hourly earnings rise 0.2%; up 4.2% year-on-year (RTS). US job openings post largest increase in two years; quits rate unchanged — openings increase 690,000 to 9.61 million while quits edged higher in Aug (RTS). Low weekly jobless claims, shrinking trade deficit boost US economic picture — Weekly jobless claims increase 2,000 to 207,000, Continuing claims slip 1,000 to 1.664 million, Trade deficit contracts 9.9% to $58.3 billion in August (RTS).

- US services sector growth slows moderately — ISM Services PMI falls 0.9 point to 53.6 in September, New orders measure drop to nine-month low, pace remained consistent with expectations for solid growth in the third quarter, Private payrolls rise 89,000; large businesses shed jobs (RTS). US manufacturing sector nears recovery; construction spending solid — ISM Manufacturing PMI rises to 49 from 47.6, New orders improve, order backlogs shrink further, factory employment increases, prices paid decline (RTS).

- US consumers cut back on credit cards as repayment charges hit record high — Rising debt burden raises fears for financial health of American households (FT). Interest rate surge drives US car loan payments to record high — One in five borrowers owes at least $1,000 a month as vehicle costs remain elevated (FT). U.S. online sales to grow 4.8% in crucial holiday season — retailers expected to go all out to woo inflation-hit consumers with even bigger discounts and promotions (RTS).

- Canada jobs, wage gains blow away expectations, up chances for rate hike — Canada’s economy more than tripled expectations by adding 63,800 jobs in September and wages continued to soar (RTS). Canadian factory PMI falls to three-year low in September (RTS).

EUROPE

- Euro zone economy likely contracted in Q3 (RTS). Euro zone retail sales fall much more than expected in Aug — retail sales fell 1.2% month-on-month for a 2.1% year-on-year decline in August (BBG). Euro zone factory activity stuck in steep downturn — Final manufacturing PMI dipped to 43.4 from 43.5 in August; France and Germany leading the way lower while Spain and Italy are pulling through somewhat less scathed (RTS).

- German government expects economy to shrink 0.4% in 2023 (RTS). German industrial orders rebound in August but outlook uncertain — “incoming orders have stabilised after a two-year decline” (RTS). Italy’s deficit hikes could threaten its credit rating, Scope says — “‘higher budget deficits this year and next could make it ineligible for bond support under the European Central Bank’s latest scheme, which would be negative for Rome’s credit profile” (RTS). Paris Commercial Property Deals Hit Lowest Level in 13 Years (BBG). Sweden Calls Real Estate Talks With Worries Mounting (BBG).

- UK house prices fall for sixth consecutive month — House prices down 0.4% between August and September (FT). UK construction activity plunges, industry survey shows — Residential index suffers biggest fall outside of the pandemic since 2009 (FT).

ASIA

- Japan’s Slower-Than-Forecast Wage Growth Supports BOJ Caution — nominal wage growth failed to accelerate from July, Lackluster pay suggests BOJ has to wait more to normalize, Households cut spending again compared to previous year; “Worker incomes are falling further behind living costs. Bottom line: The data bode ill for household spending — and reinforce our view that a BOJ pivot away from stimulus is a long way off” (BBG). Japan service PMI slows down in September — 13th month expansion but at the slowest pace since the start of the year hurt by slower new business and a stalling in export orders (RTS). Foreign Investors Dump Japanese Stocks for Second Week (BBG).

- S.Korea factory output posts biggest gain in over three years boosted by chips — industrial output index rose 5.5% in August from the previous month on a seasonally adjusted basis after a 2.0% fall in July, contrasts with a median 0.2% fall forecast (RTS). S.Korea factory activity shrinks again in Sept but at mildest pace in 15 months (RTS).

- RBA held interest rates steady at 4.10% for a fourth month and showed no urgency to hike again (RTS). RBA Says Share of Borrowers in Early Financial Stress Is Growing (BBG). New Zealand House-Price Slump May Be Over, CoreLogic Says — Prices steady in September after 17 straight monthly declines, ‘Housing market confidence seems to have turned a corner’ (BBG).

- India’s RBI holds rates; signals tight policy on inflation worries — India cbank keeps interest rates steady for 4th straight meet, RBI may sell bonds to keep liquidity tight as inflation clouded, Reiterates its inflation target is 4%, not 2–6%, Benchmark yield sees sharpest jump in 14 months on prospect of bond sales (RTS). Goldman Is Cautious on ‘Expensive’ India Stocks Before Polls (BBG).

- China’s Golden Week Tourism Nudges Past Pre-Pandemic Level — Weeklong holiday spending was up 130% on 2022’s total, Domestic trips fell shy of tourism ministry’s estimates (BBG). China Markets Face Choppy Return From Holidays as Risks Abound — ,Mainland markets reopen Monday after the Golden Week holidays, Traders to weigh global market swings against spending boom (BBG). Macau Casinos Boom as Chinese Tourists Flood in for Holiday — Tourist arrivals during long holiday reaches 84% of 2019 level, Gambling hub is rolling out major events to attract tourists (BBG). Hong Kong to Pause Selling Commercial Land as Market Falters (BBG). Hong Kong Home Rented Out for $140,000 a Month Despite Market Downturn — Luxury residence at №11 Plantation Road is owned by Wharf, Expert sees potential for more demand from mainland buyers (BBG).

EQUITIES

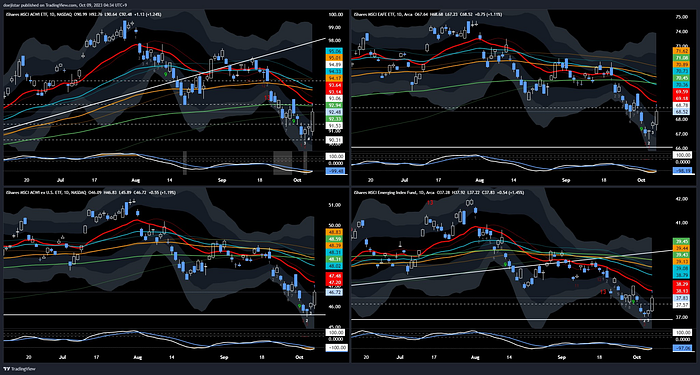

MSCI indices price action convincingly to more upside — daily extreme oversold and a long-legged doji wicking off the weekly 3sd band.

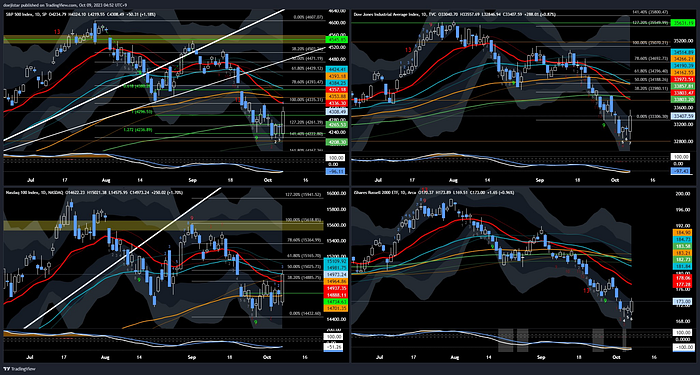

Bounce was led by Nasdaq while Dow and Russell charts look great and ready to participate.

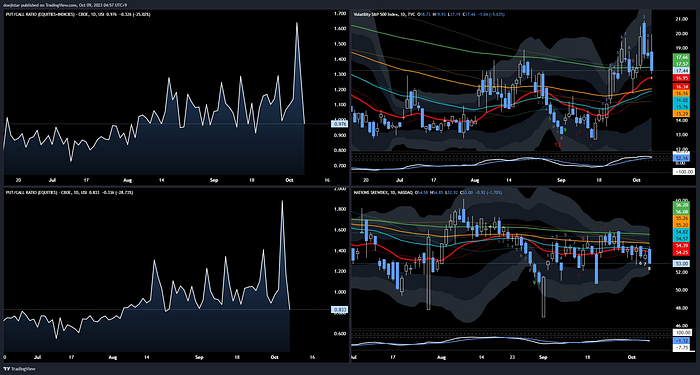

VIX easing off along with put option premiums after the sharp reversal in Put/Call ratio which is, at the stock level at the lowest since late August.

Refinitiv’s most shorted stocks index also showing solid signs of bottoming and looking ready to get a short-squeeze on — when the shitcos rally, you know that risk appetite is back.

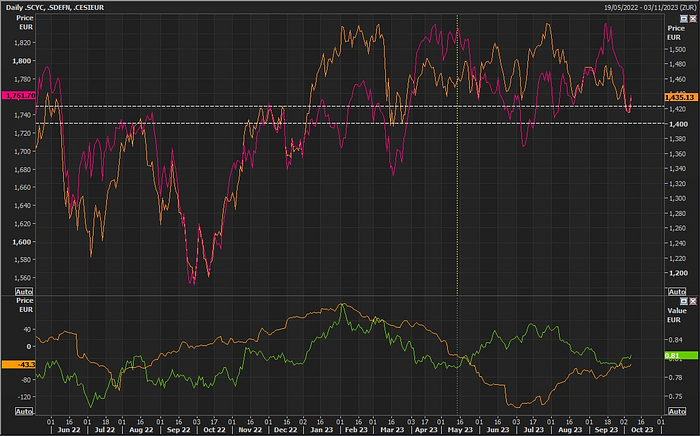

European stocks also showing hints of improved confidence bouncing from this key region. Green line shows the spreads between Stoxx600 Cyclicals (Orange) and Defensives (Red) and is looking up along with the EUR economic data surprise index.

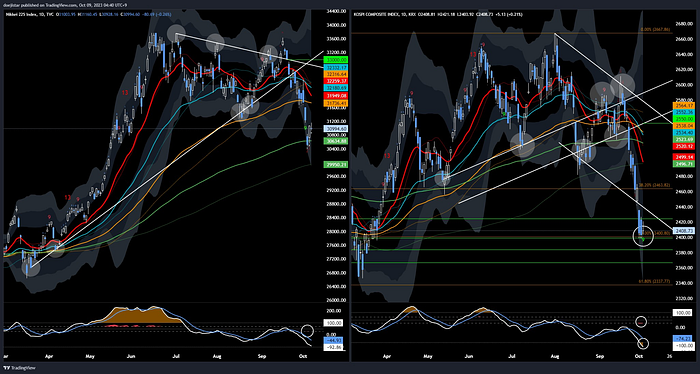

Asian markets were extremely weak in recent weeks and showing some positivity from extreme oversold levels — NIKKEI with a decent bounce off the 200ema and KOSPI demark 9 countdown hinting a potential reversal at the key 2400 pivot level.

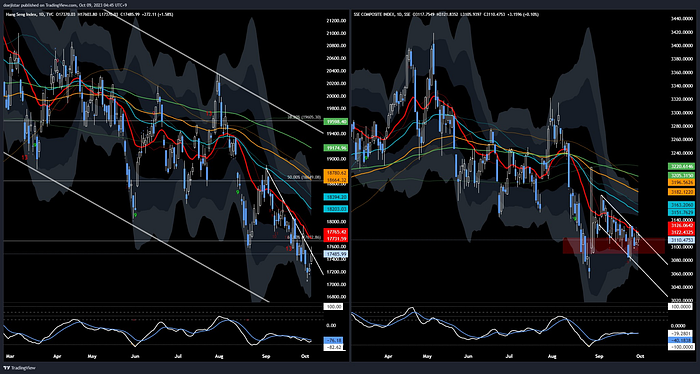

China also showing potential for a bounce back with the Hang Seng looking to break trend with MACD attempting to turn positive, and the consolidation in Shanghai composite is starting to look like a coil-up and ready to break higher when they return from their long holiday break.

COMMODITIES

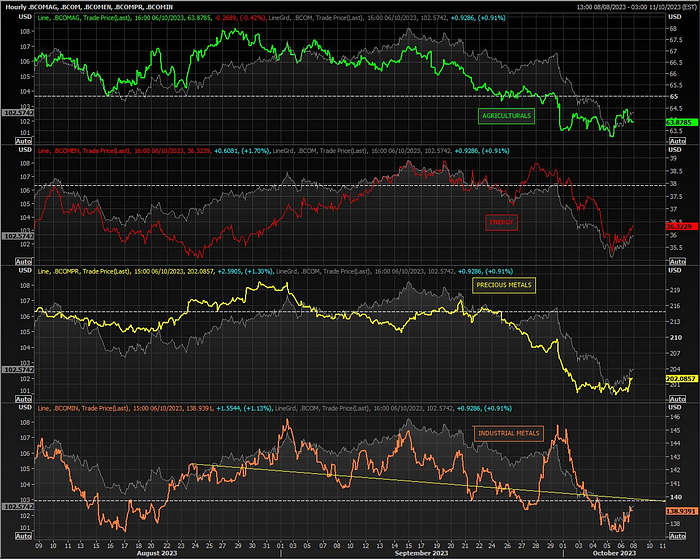

Commodities slumped into September and was beginning to look quite oversold last week, particularly for metals. As we do have September PPI and CPI this week and the concern the Oil squeeze would pose upside risks to those prints, the Energy was shy of +4% last month while Agricultural and Industrial metals was mostly lower during that period.

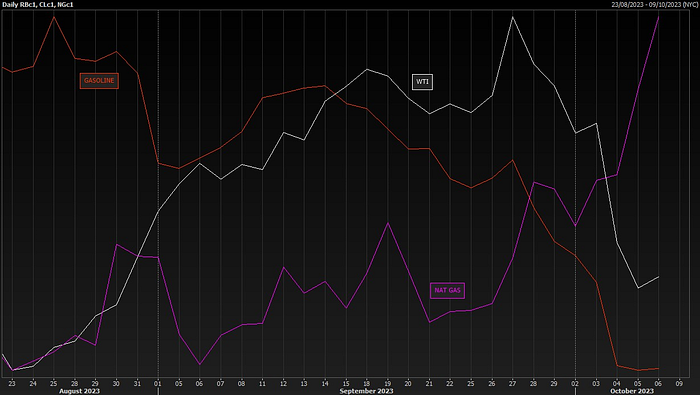

Further, Gasoline prices slumped -6.91% while NatGas rallied only +2.71% last month which doesn’t make me overly concerned about upside surprises to this weeks data. Any hawkish reactions is most probably a fade anyway.

I continue to favour upside in Precious metals from this area and have covered the WTI short from 93.50 around the 82 handle as I think the resilience of last week’s data could help to support the demand side of the story. I now prefer proxies such as petro-currencies NOK CAD and energy stocks to play the bounce instead of outright longs on WTI.

CURRENCIES

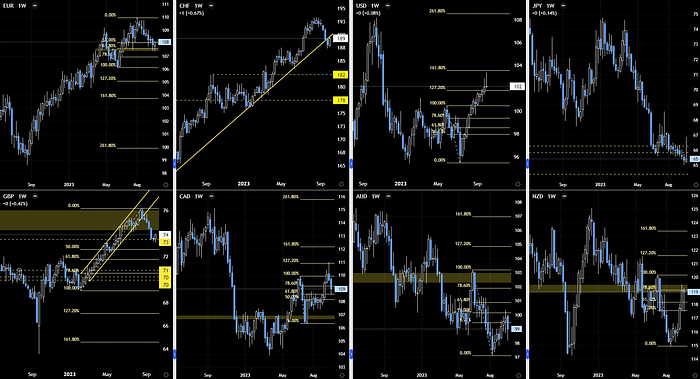

EUR and GBP are reacting nicely to the pivot level while the USD has sharply rejected the 61.8 fib extension .I also continue to favour EURUSD and GBPUSD longs as a way to fade the USD (fading the most hated against the most liked USD).

I also like CAD given the strong jobs report and potential for a bounce back in Crude prices, while JPY remains heavily disliked in my book despite all the talk of an MOF/BOJ intervention or ‘rate check’ rumours.

Overall, charts look poised to keep pushing next levels and I’m quite happy to sit back and let the momentum play out til the inflation data and treasury auctions.

That’s it for now — good luck trading! //