2024.10.13 Weekly

Growing up as a kid I wasn’t allowed to watch TV no less own a gaming console so every time I had the opportunity to go a friend’s house, I took full advantage and played as much video games as I could. One of them — probably showing my age here, was to play NBA Jam on the Supernitendo (I think it was) where the key strategy to widen the scoring gap against your opponent was to get one of your players on a scoring streak. Doing so would get them “on fire” making the player virtually undefendable for a certain period of time. And you could tell you were close as the in-game commentator would say “he’s heating up!”.

That’s how I see inflation pressures in the US at the moment with a streak of stronger inflation and wage prints appearing. In addition to wage growth now running at a 3-month annualised rate of 4.3% as highlighted last week, latest inflation data suggests price pressures have not dissipated as implied by Powell and assumed by the market. These risks still look very underappreciated by both the Fed and the market that sees a pace of roughly 30bps per quarter til the end of 2025, even after the big post-NFP adjustment that saw the implied rate for the December 2025 contract move up 50bps over the past month.

Based on the data pointing to upside risks to inflation, a more reasonable baseline to me would be a gradual pace of 25bps per quarter that would see the Fed funds rate at 3.58% by the end of 2025 (shaded on the chart). This would in fact be slower than the pace implied by the Fed’s median projection of 3.38% by the end of 2025 (dashed horizontal line). The above baseline pace begins with the assumption that we will see just one more 25bps for the remainder of the year, which is at odds with the market that is still priced in for 25bps in each of the last two meetings:

Powell in his FOMC press conference led us to believe the committee was fully behind the decision to cut 50bps, the Minutes of the meeting released last week hints that the committee may not be fully on board with rate cuts in quick succession. Anna Wong with this deconstruction:

FOMC minutes basically showed the Powell basically pushed the committee to do 50 bps in September. Key passage is this (with quantity words highlighted): “Some participants emphasized that reducing policy restraint too late or too little could risk unduly weakening economic activity and employment. A few participants highlighted in particular the costs and challenges of addressing such a weakening once it is fully under way. Several participants remarked that reducing policy restraint too soon or too much could risk a stalling or a reversal of the progress on inflation. Some participants noted that uncertainties concerning the level of the longer-term neutral rate of interest complicated the assessment of the degree of restrictiveness of policy and, in their view, made it appropriate to reduce policy restraint gradually.”

In equation form, it can be summarized as:

In 50 camp: SOME + A FEW

In 25 camp: SEVERAL + SOMESEVERAL+SOME >>> SOME+A FEW

25 bps >>> 50 bpsQED Will the opposition demand their pound of flesh in the future?

Bostic in his interview with the WSJ said that while he fully supported the 50bps decision, he said he was “totally comfortable with skipping a meeting” as he was already penciled in for 75bps for 2024, and with 50bps already done “that already signals that I’m open to not moving at one of the last two meetings if the data comes in as I expect”.

I think Anna Wong is asking the right question of whether some of the committee members will “demand their pound of flesh” over the next meetings — i.e. seek a pause. Recent data certainly warrants it in my view, and as I have argued for before the September meeting, there was absolutely no need to rush into a 50bps cut that could risk sending wrong signals to the market — that the Fed was effectively declaring victory on inflation and signaling its intent on getting back to neutral quickly. With growth, supercore and wage inflation in reacceleration, I’m pleased to see I’m in good company — Vincent Deluard in his thread, who by the way has had an excellent handle on inflation this whole cycle, concludes:

The Fed was crazy to declare victory on inflation.

The 50 bp cut was a huge policy mistake, a la Trichet

Inflation Is a Process, Not an Event

….and it’s not over.

Not only do we look mispriced at the front end of the curve, if the recent reacceleration of growth and inflation is sustained, we should see much higher yields than many sell-side reports have forecasted — most of which seems to see the 10yr stay around the 4% mark over the near-term, then coalesce towards the mid 3s by the end of 2025. I think it is more likely that the 2yr stays close to the 4% mark and the 10yr making its way towards the mid 4s by the end of 2025. This mispricing presents risks to Equity market valuations and extended USD strength.

DATA REVIEW

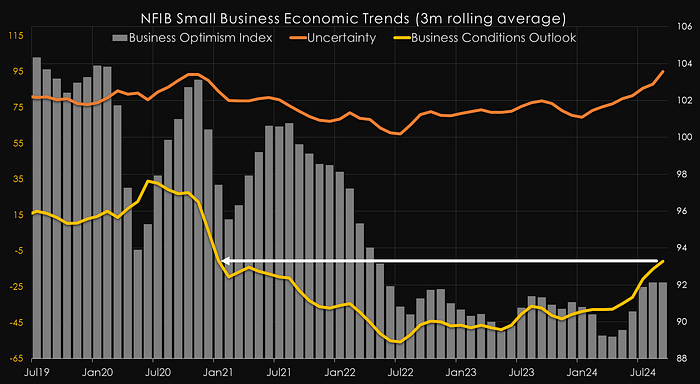

NFIB Small business optimism was below expected but recent trend remains positive — especially on 6-month business outlook which is the least negative since January 2021 on a 3month rolling average basis.

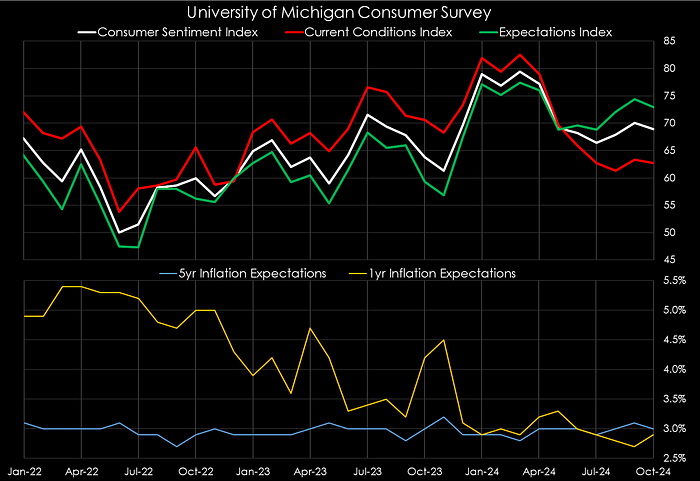

UoM survey was weaker all missing expectations except for the 1-year inflation expectation jumping higher to 2.9% above the expectation to remain unchanged at 2.7%.

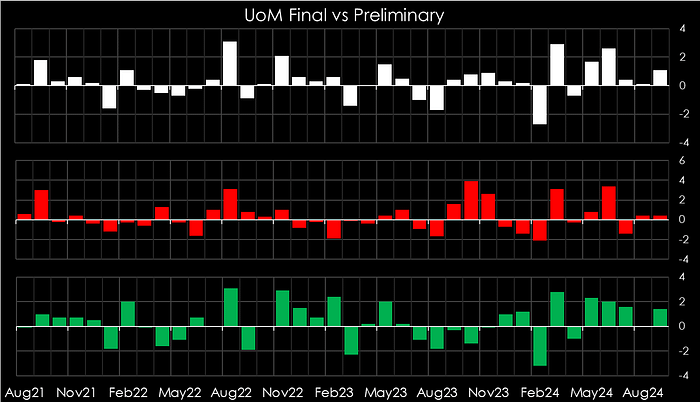

I also seem to recall that Preliminary UoM releases have generally been more pessimistic than the Final, and upon checking, it has indeed been the case particularly for the Sentiment and Expectations index.

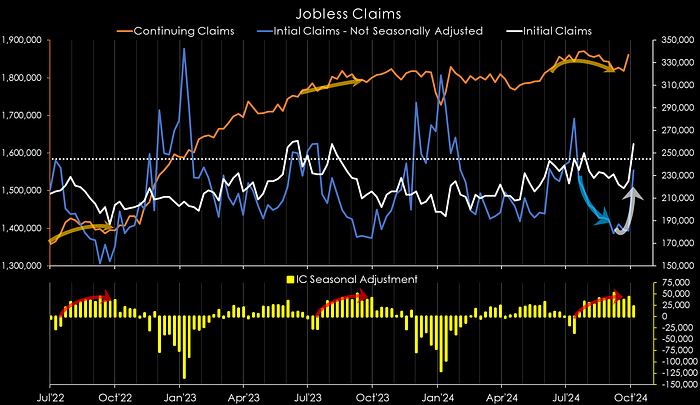

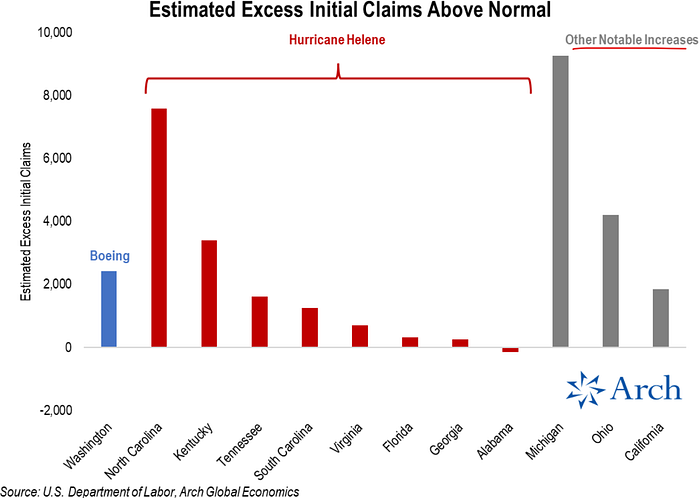

Jobless claims shot up roughly 30k more than expected for both initial and continuing claims. Initial claims equaled the Aug-2023 high at 258k, now above the pre-pandemic 5-year average (dashed horizontal line). This was initially thought to be have been due to the Hurricane impact, but as Parker Ross explains in his thread, that there were “substantial increases in claims outside of these widely anticipated transitory factors”.

Some observations he’s highlighted:

- Michigan Initial claims jumped more than any of the hurricane-impacted states. 130% higher than normal for the 40th week of the year.

- Ohio Initial claims surged by 4.3k, 56% above normal. Some of this is likely related to the Stellantis layoffs.

- Likely to see further increases as the full impact of Hurricane Helene is processed. We’ll also start to see Hurricane Milton impacts in the weeks ahead, which will leave the labor market outlook muddled.

- Challenges with the seasonal adjustment factors will also put upward pressure on claims into year-end, most notably for continuing claims.

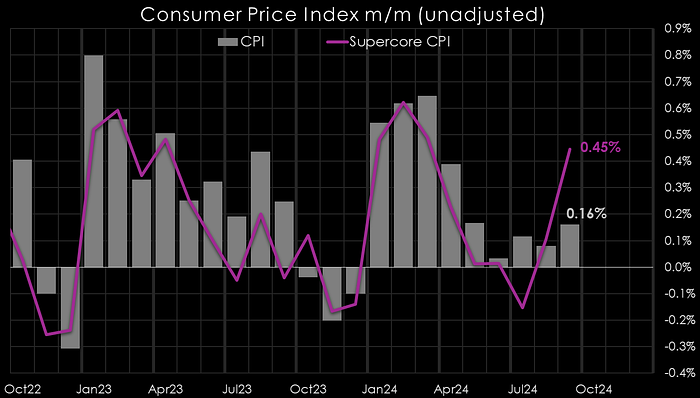

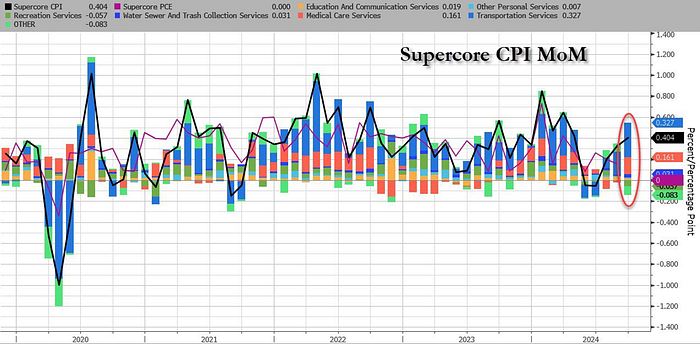

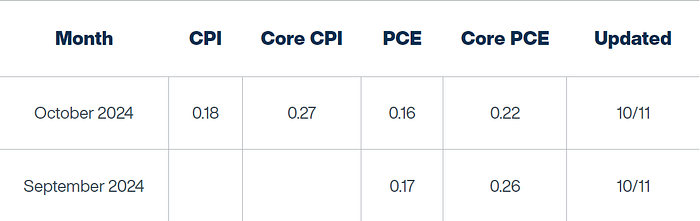

CPI came in hotter than expectations at 0.2% (0.16% unrounded) vs 0.1% expected, and 0.3% vs 0.2% expected for core. What is particularly concerning about this report is Supercore (which excludes all volatile items and Shelter) bouncing back sharply over the last 2-months. This suggests price pressures are broad, and though unlikely to maintain this monthly rate of increase, 0.45% m/m is huge, annualises to over 5% for context.

Most of that increase came from pervasive components such as Transportation services (Airfare and Auto-insurance) and Medical care services. Outside of core, grocery prices jumped at the fastest monthly pace since the beginning of the year, and Energy services rose for the time in 5 months. Some items that increased the most over the past month:

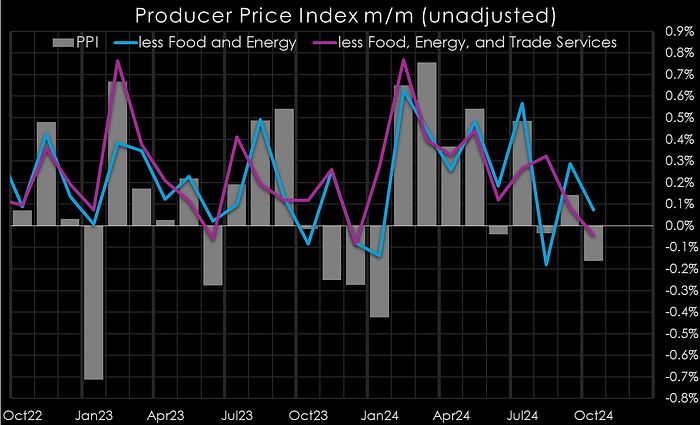

Despite the hot CPI report, producer prices on a non-seasonally adjusted basis was softer. Even so, after both inflation reports, the Cleveland Fed inflation nowcast now has September Core PCE at 0.26%, up from 0.22% prior to the two reports.

A concerning data week for the Fed overall. On top of the jobs report showing wage growth acceleration a week earlier, there was a spike in unemployment claims that was not wholly attributable to transitory factors, and the CPI report is showing services inflation to be broad and in reacceleration also.

CHINA

There was some anticipation last week that China would make more stimulus announcements at the Saturday policy briefing, but once again, it was light on detail and proving to be a disappointment against the high level of optimism around China’s so-called ‘whatever it takes’ moment.

Quoting the highlights from Reuters: China flags more fiscal stimulus for economy, leaves out key details on size:

- China finance ministry says will ramp up debt issuance

Size of fiscal stimulus unclear, expected to unnerve markets

Beijing says will support indebted local governments

Will offer subsidies to low-income people, recapitalise banks

Pledges measures to stabilise property markets - “The strength of the announced fiscal stimulus plan is weaker than expected. There’s no timetable, no amount, no details of how the money will be spent”. “If that’s what we have in terms of fiscal policies, the stock market bull run could run out of steam” says one Fund manager.

- Some remain more optimistic saying that “Investors will need to be patient” and while “Potentially some event money might be disappointed and remove some bets on the headline numbers not meeting high expectations… A sustained rally driven by the China household has the foundations for success … we are early in this process and the risk is the possibility of flawed execution or not communicating things well. The structural story remains compelling though.”

Somone who is very much uncovinced with China’s policy stance, and still remains very negative on the China macro outlook is Brian McCarthy — an ex-Manager of the China-focused Nexus fund that has accurately timed China’s deflationary bust during the mid to late 2010s. A colleague shared some keynotes from his recent presentation — long-story short, he doesn’t believe in an immediate revival of the Chinese economy like many would have you believe, nor does he see Xi Jinping pull off his plan to transition the economy from the failed growth model of infrastructure spending to high-quality (productivity growth) development plan:

- Unless China departs from the principles and directives (that focused on ‘short-term pain’ and ‘incremental policies’) laid out by Xi and the CCP since March, China is unlikely to deliver bazooka-styled stimulus that would have to be in the order of 5–10 trillion Yuan.

- Sees significant scope for disappointment and believes the next phase of this story is domestics piling in and global hedge funds being happy to be their supply.

Plenty of food for thought, and as someone who’s been looking for a revival in Chinese equities via Alibaba HK:9988, its left me thinking about a partial or sooner exit than I had long envisioned for that holding.

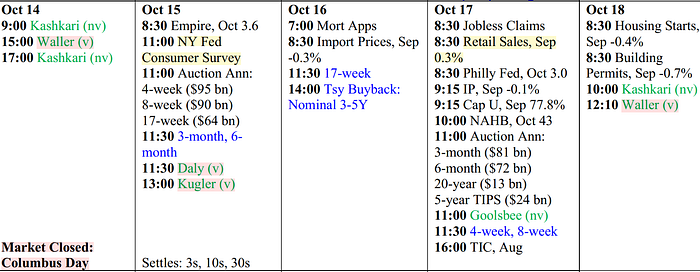

LOOKING AHEAD

Fed speakers, NY Fed consumer survey (1yr inflation expectations) and Retail sales the main events in the US, elsewhere:

- Tue: UK employment data, FRA/ESP CPI, ZEW, Canadian CPI

- Wed: New Zealand and UK CPI

- Thu: Australian employment data, ECB

- Fri: China UK and Candian Retail sales, Japan CPI

EQUITIES

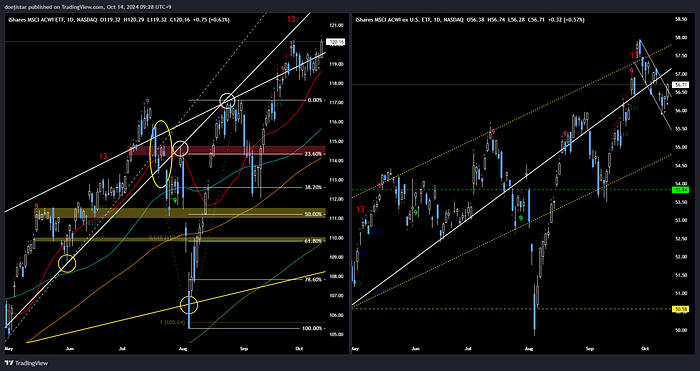

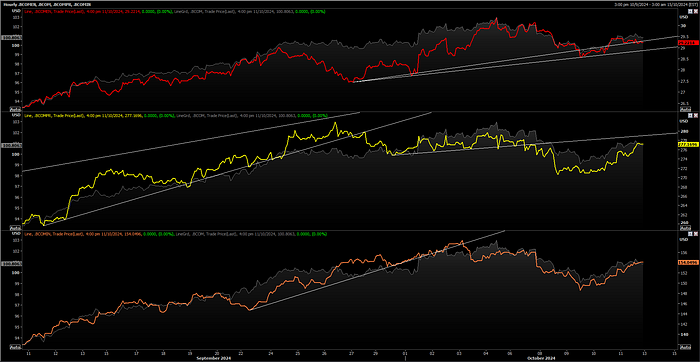

Global equities put in a strong week and setting itself up for more gains. All Countries World Index (ACWI) has pushed on above its upper trendline that, for the most part, looked to be capping the rally until the Friday move; and the ex-US index (ACWX) is breaking out its bull-flag structure.

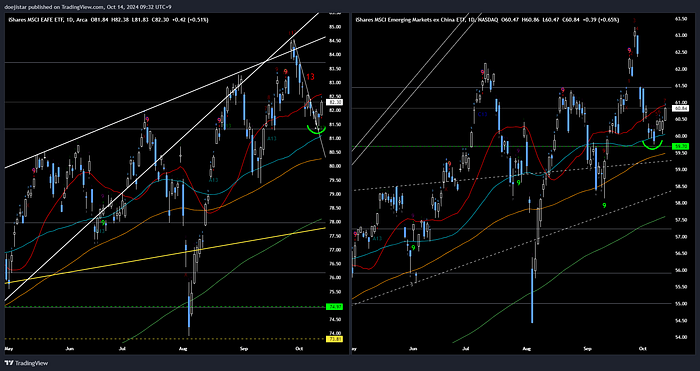

Developed markets (EAFE) and Emerging ex-China (EMXC) has put in a nice bounce but faces the 20dma overhead.

China equities put in a huge reversal last week after a monster rally. It looks set to consolidate lower and remains to be seen whether it can recapture those highs anytime soon, especially with the stimulus news falling short of lofty expectations.

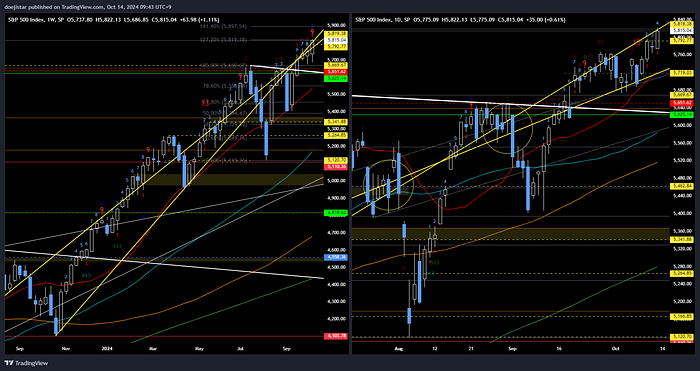

SPX finished strongly after a weak start to the week where I had thought it is becoming unsettled by the big move in yields. Nevertheless, it’s closed at an interesting spot with a weekly demark 9 countup printing at the 127.2 and 161.8 extensions of the last two swings, as well the well-respected trendline. ES and NDX also with demark countups on the daily chart:

I’m sure many have been made aghast at my intentions to sell SPX, but I’m looking to build a position trade that I think has a good chance of working out over the next few weeks, and I think those are good levels and technical reasons (albeit without confirmation) to do so around here.

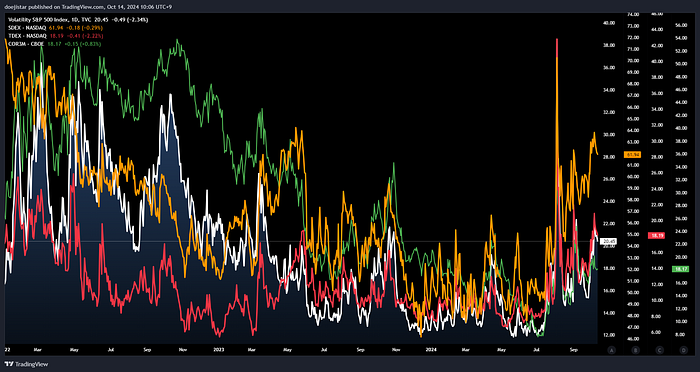

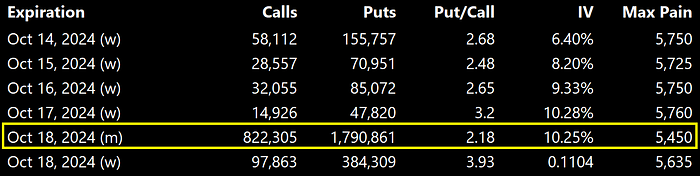

Skew is still quite high as indicated by the Orange line and the high put/call ratios. Market is presumably very well protected on the downside and possibly the reason why equities have not been able to sell off, pinging back to the upside after every brief period of intraday selling.

The options market is clearly concerned about the downside and perhaps OPEX at the end of this week will allow the market to roam a little bit thereafter.

Looking at the Friday expiry, there is a huge chunk of itm-calls between of 5600 and 5800 strikes rolling off this week. A lack of upside momentum and SPX trading below 5750 again (taking out Thursday and Friday lows) would be a early signs of upside exhaustion, pariticularly if it happens ahead of schedule as there is some put blocks to provide some ammunition to downside moves.

COMMODITIES

I noted the potential for a reversal in commodities last week with the reemergence of USD strength, and the commodities index printing an inverted hammer close with RSI coming of extreme overbought. It’s retraced higher after a strong early week reversal, but still looks to me like it is on a consolidating trend lower as global industrial data being weak and China stimulus news underwhelming won’t be of much help.

Oil has seen some headline-induced selling last week but I’m encouraged by the fact that it has been able to hold up if not recover some of those moves. Energy sub-index continues to maintain a positive bias, but I do have some technical concerns for Oil — more below.

Precious metals sub-index has virtually recovered the flush lower. I’ve got the initial adjustment to US rates and dollar call right and should have gone flat once the move came through, but ended up sticking around too long looking for a bigger move and ended up leaving plenty on the table. Flat on precious metals, on not much of a view at this point.

While still focused on tradeable dips in Crude, I am turning a little more cautious here after seeing a rejection of the trendline and both the 20 and 50wma last week. RSI has also stalled at the 50 mid-line and unable to produce a break higher.

Also have my eye on Copper shorts which looks at risk of breaking down towards 4.25 with RSI heavy just above the 50 mid-line. I would be keen to sell any rallies into 4.45-50 if possible targeting the 200dma.

RATES

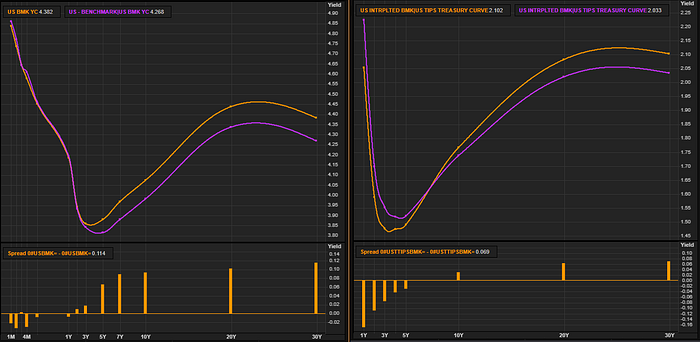

Treasury yields were higher last week with the biggest change coming in the longer end and higher inflation breakevens across the curve.

2yr and 10yr note futures are looking oversold while finding support at the 200dma. There are a lot of Fed speakers on the calendar to start the week but I don’t expect them give the bulls much joy, so it will likely have to be in the form of a soft retail sales report to solidify a base and short-term rally. Conversely, the 10yr is at a point of potential point of pain such that if retail sales comes in hot, we could see an unsettling move in the 10yr yield higher towards 4.25%.

CURRENCIES

My focus has been entirely on the USD in FX, via short EURUSD GBPUSD NZDUSD, and long USDJPY USDCHF — full run down on these under this thread:

After reaching some initial targets, the assessment I’m having to make is what is the dynamic risk/reward from this point on. In other words, how much profit potential do I see versus say a 1% trailing stop risk?

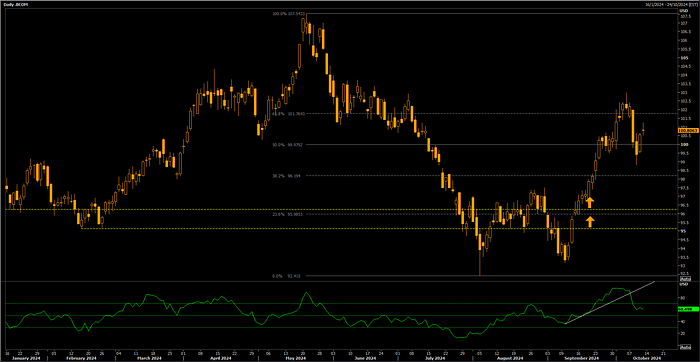

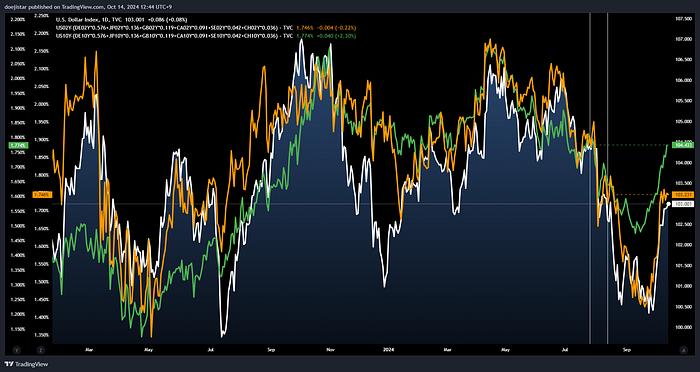

Looking at the 2yr and 10yr DXY-weighted yield spreads, we can that the DXY is just about fairly valued if not slightly undervalued to where the 2yr spread was last at current levels, whereas the DXY was much stronger when the 10yr spread was last at these levels during late July.

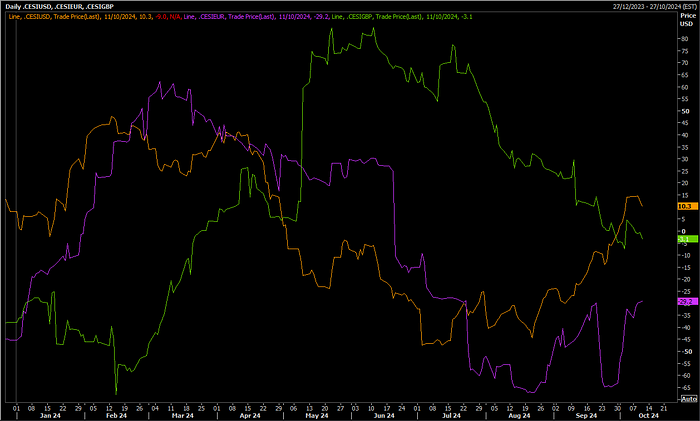

Looking at Economic surprise indices for US (Orange), Europe (Purple) and UK (Green), US has a noticeably strong upward momentum versus the rest since July, which is reflected by the strong 10yr spread in the chart above.

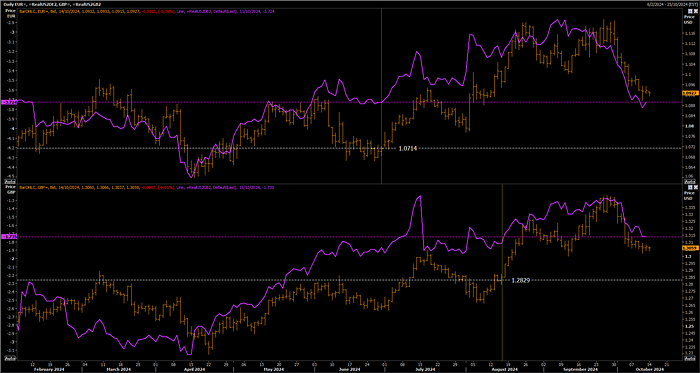

Looking at where the 2yr real rate spread, both EURUSD and GBPUSD still look quite strong with the pairs trading around the 1.07 and 1.28 handles respectively the last time the spreads were at current levels.

Based on USD yields spreads, I think USD has scope to extend gains. Looking at Central bank considerations — ECB decision this week, the BOE on Nov-7th followed by the FOMC on Nov-8th:

- The ECB has a chance of a 25bps cut this week particularly if they are becoming concerned about growth. While some inflation pressures remain, Eurostat Core CPI Flash Estimate was at 2.7% while the headline CPI estimate was at 1.8% suggesting there is some room to cut the deposit rate to 3.25%. Market is pretty much nailed in for a cut at each of the next 2 meetings but I think that’s a close call. EUR could see some short covering this week if the ECB goes for the hold (or cuts with the signal they will continue at a much slower pace from hereon). I don’t expect rallies to last however given structurally weak fundamentals, and China (a big market for Europe) underwhelming with their stimulus announcements.

- BoE have also been hinting a pivot with Andrew Bailey in an interview with the Guardian suggesting that a ‘more aggressive’ path for cutting interest rates was possible if inflation news stays positive — that’s the first time we’ve heard anything like that from Bailey. While core inflation remains sticky at around 3.5% y/y, Inflation at 2.2% y/y for the last two prints and BoE interest rate at 5%, I think there is a good chance we see a cut in November. UK data is also cooling off from a strong early year run, and should this week’s UK employment and CPI add to that picture, I don’t see GBP regaining much ground.

- The FED as covered earlier may have forced themselves into a pause at the next meeting, which could result in another repricing leg with the market nailed in for two 25bps cuts til year end. Plenty of Fed speakers on deck along with retail sales this week to assess whether current USD momentum can hold up.

Lastly for USDJPY and USDCHF — I don’t see how those currencies can compete against the USD whose carry is likely to remain attractive for some time. BOJ meets at the end of the month and they are clearly not in any hurry to raise rates. As for the SNB, while their next meeting isn’t until December, Swiss monthly inflation has been printing flat to negative since July so I am not at all concerned about CHF upside risks either. So it should all boil down to US retail sales this week and potentially hawkish Fed comments.

Going back to the question of assessing my risk/reward from current levels for the heavily long USD book, based on the assessment above, I see at least 1% and as much as 2–3% upside potential in EURUSD and GBPUSD, a continued drift higher in USDJPY and USDCHF, and I think a 1% trailer on each from current levels offers decent risk reward at worst case. To touch on NZDUSD short, I follow my view on equity risk appetite of which I think will start to see it weaken over the coming weeks. Without the tailwind from a continued risk-on rally and China stimulus, I think it will be difficult for NZD to find a meaningful rally.

— — — — —

Thats all for now. Good luck trading!