2024.09.30 Weekly

Normalisation…

There’s been plenty of focus on the latest Conference Board data as the labour differential has historically tracked unemployment virtually to a ‘T’:

The chorus for more aggressive easing sung louder last week on this data point and looking at that chart — the sharp turn certainly looks alarming. What’s interesting is that the timing has not been well-aligned with the unemployment rate responding slowly to that sharp turn and I think this raises some interesting questions on why that could be and how it might need to be interpreted differently. In other words, context is important.

First, the slow pick-up could be explained by interest rates not having the same impact on economic activity as it did in previous cycles. Economic activity (e.g. GDP) has proved resilient along with wage growth and consumer spending, that will be further supported by inflation-headwinds dissipating and the Fed responding to that. Secondly, as the data review have shown — 1) the labour market is yet to do anything more than normalising and 2) overall data has yet to point to a slowing of economic activity.

Taking all the above into consideration, I don’t see the need for the Fed to follow up with another 50bps over the usual pace of 25bps per meeting, that being said, I also don’t see a huge difference between doing another 50bps and holding for a couple meetings or, going with 25bps and keeping each meeting live either. Regardless of either of those points however, market expectations still look ‘excessively-dovish’ and that is making yields and dollar looking mis-priced and would have serious implications over the near to medium-term trading environment.

Macro data review

CB consumer confidence index dragged by down Present situation index, which was driven by consumers turning net-negative on Current business conditions and, less optimistic of Current labour market conditions which is stirring up some debate on whether the Fed should continue with their 50bps clips as the labour market differential (blue-line, top-panel below) tracks the Unemployment rate closely.

Looking at the 6-month outlook, consumers remain optimistic on business and income expectations with the differentials looking healthy by recent standards. As the survey cut-off period ended just before the Fed delivered the 50bps cut, I’d lean towards confidence stabilising than deteriorating going forward.

Returning to the point of labour market differentials (jobs “plentiful” minus “hard to get” in the top-panel) — while this differential closely tracks unemployment historically, I think assessing the context is important. That context being that we have rarely had a labour market as tight as it was post-pandemic where ‘plentiful’ was extremely high and ‘hard to get’ extremely low, thus this narrowing being more of ‘trend normalisation’ (‘plentiful’ coming down faster than ‘hard to get’ is rising), rather than a ‘harbinger of weakness’ as it has been historically. Meanwhile, though we did see a slight softening in the 6-month differential the last period, it remains far less pessimistic than the earlier part of the year, and income expectations remains surprisingly resilient.

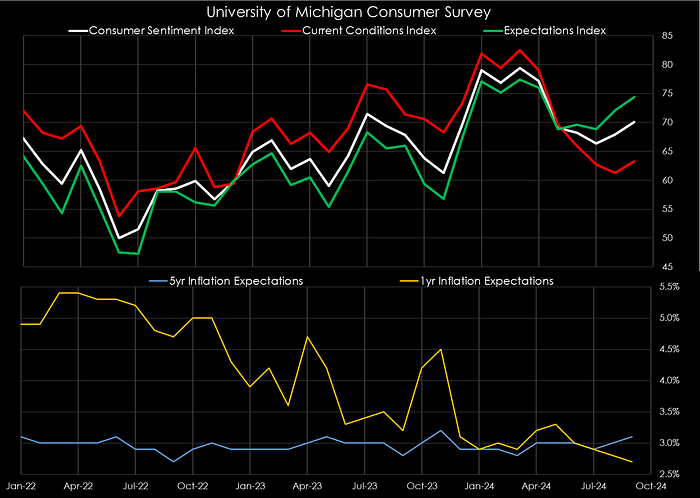

UoM consumer survey beat expectations across the board:

- Consumer sentiment index was revised upwards to 70.1 from the preliminary 69.0 which was higher than the initial forecast of 68.3, and prior month of 67.9

- Current conditions index also revised upwards to 63.3 from the preliminary 62.9 which was higher than the initial forecast of 61.5, and prior month of 61.3

- Expectations index also revised upwards to 74.4 from the preliminary 70.3 which was higher than the initial forecast of 71.0, and prior month 72.1

- Inflation expectations unchanged from the preliminary reading, but interestingly the 5-year expectation ticked up the highest reading in almost a year (Nov’2023) to 3.1%, above the 3.0% initially expected.

Overall, consumer sentiment is notably weaker but future expectations remain relativty healthy. While UoM does have a tendency to lag and remain more optimistic than the CB data, much of this stark contrast stems from the continued narrowing in labour market differentials which, I hypothesised above as reflecting normalisation than inherent weakness.

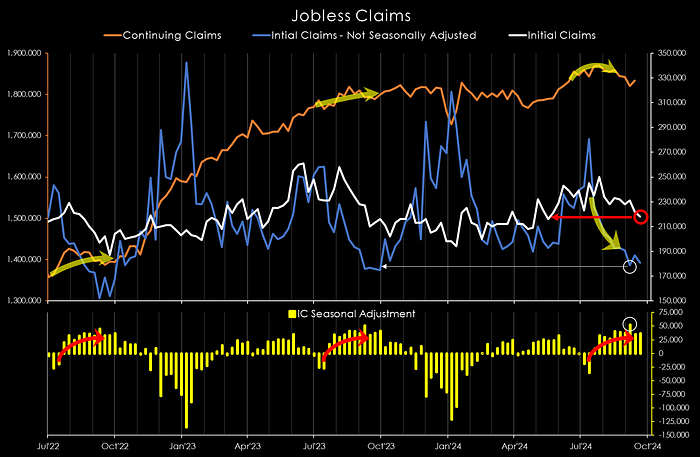

Initial claims hit a new 18–week low to 218k and widening the gap below the pre-pandemic 5-year weekly average of ~245k. This is consistent with the idea that Conference Board labour market differentials may not be something to be concerned over for the time being.

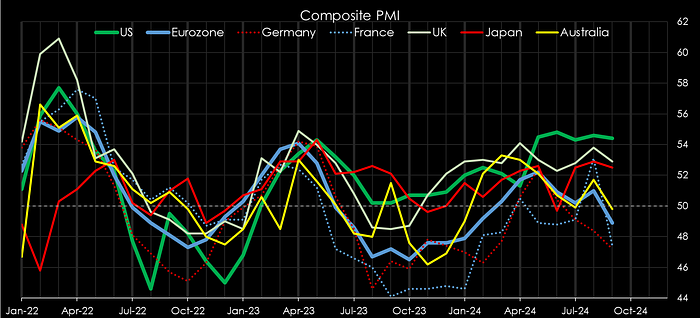

Preliminary Flash Composite PMIs have turned lower across the board but notably much more for Europe and Australia, both of which are in contraction (below the 50–line). US is still head and shoulders above and maintaining a stable rate of expansion over the last 5-months.

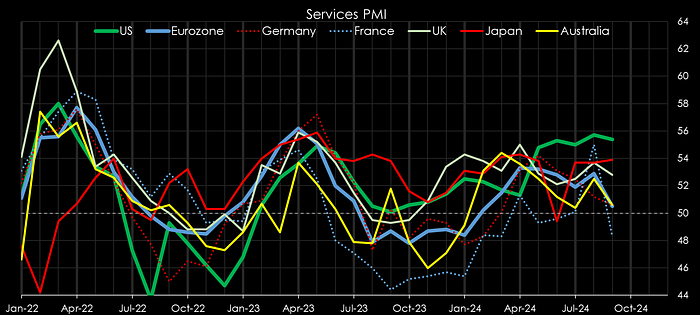

Services PMI remains robust for the US and Japan, while others have softened. Most notable is France diving below the 50-line.

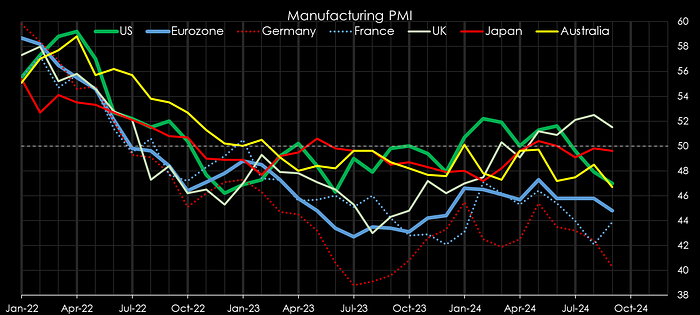

Manufacturing ytd slump continues. UK the odd one out but the expansion leg may start to look like a period of normalisation going forward after a long downturn. German manufacturing slump accelerated even further.

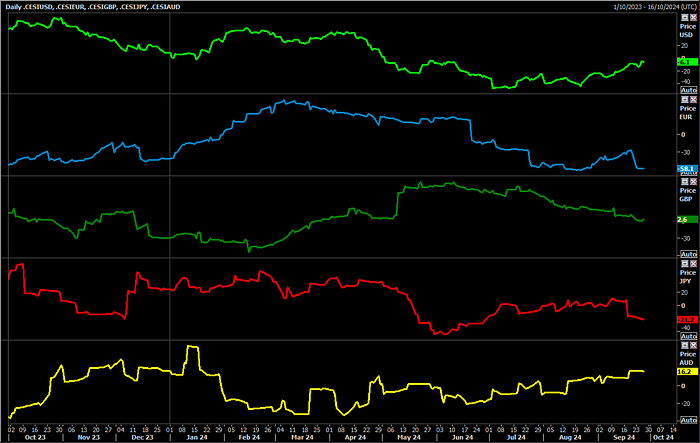

Citi Economic Surprise indicies (from top to bottom): US index continued to go higher after turning a corner earlier in the quarter, Europe continues to fall short of expectations, UK had a good run of data but no longer exceeding expectations in Q3, Japan dropped recently to finish at the lowest level of the quarter, and Australia continuing to show resilience.

X-asset review

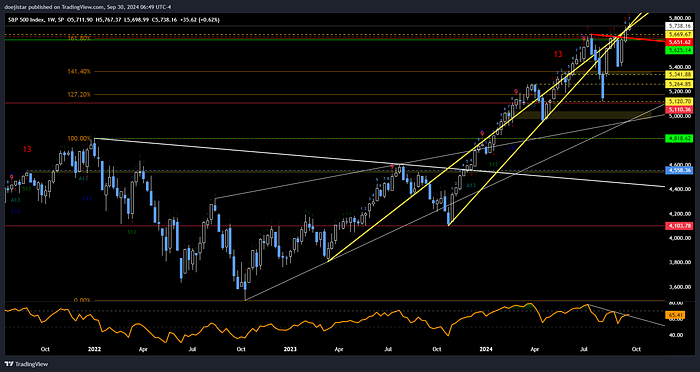

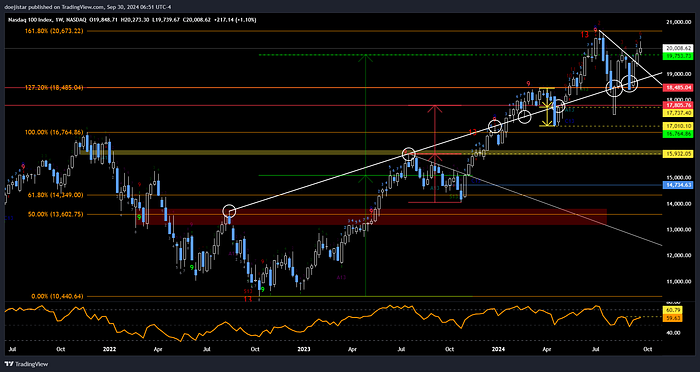

SPX in an interesting spot here where a couple trendlines meet after extended above the July all-time-high. No doubt the chart is bullish after the breakout but 1) last week’s follow through was somewhat unimpressive, and 2) RSI still remains in a trend of lower highs and lows.

NDX with similar observations after the breakout. 19,750-950 area will need defending this week to maintain the upside bias but there daily chart is showing a lot of intraday chop in the latter half of September, which to me is subtly hinting buyer exhaustion.

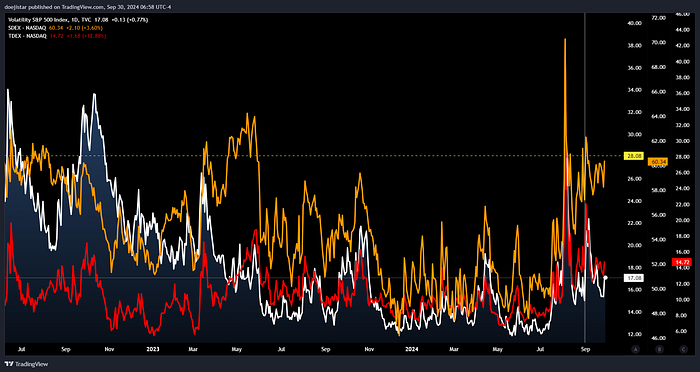

Equities Volatility via the VIX index has settled lower through the month of September but SDEX (a measure of put premiums, i.e. demand for downside protection) has stayed elevated throughout. I expect volatility to be more elevated as we progress through October as approach closer to elections. Equities generally do not like periods of uncertainty and downside hedging will likely shift gamma positioning more negative.

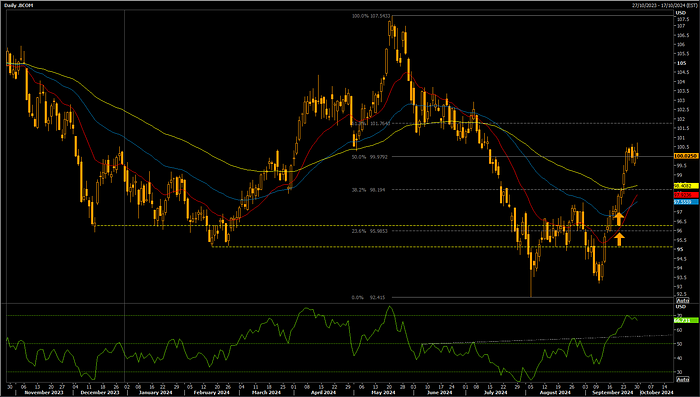

Bloomberg commodities index continued their upward correction I’ve been making a case for in recent months. It is now sitting around the 50% retracement level with RSI fading off the 70 level last week showing some signs of buy exhaustion on this up-leg.

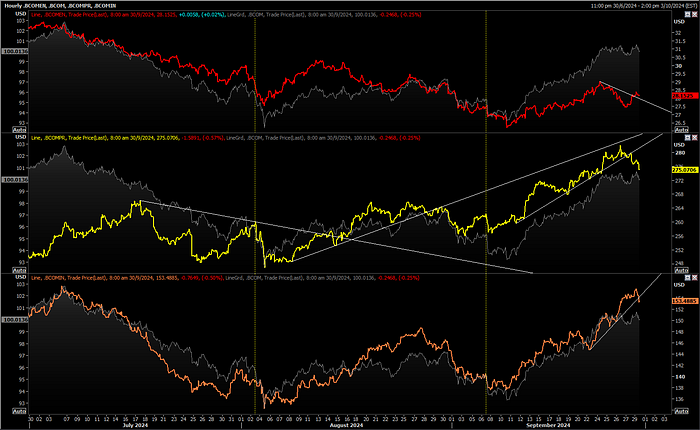

Energy / Metals subindexes exhibiting some clear near-term risks — Energy looking to build on the September bounce which given the escalation in geopolitical risks would seem a reasonable possibility; Metals looks ready to pullback after a strong rally last week, and Caixin PMIs earlier today will probably stall the bullish momentum for now. I’ve been a big advocate of looking to short the precious metals rally, and it finally looks like it may have turned a corner.

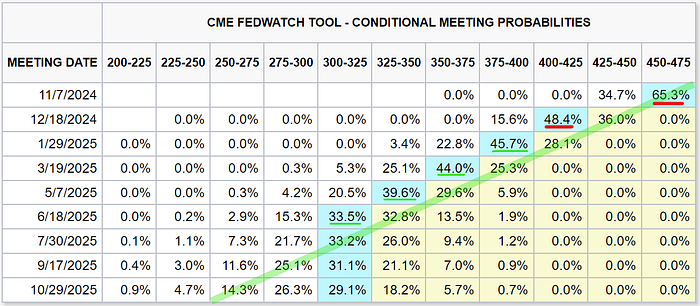

Fed funds futures are still leaning towards another 50bp cut by year-end expecting that to come at the December meeting. While it’s unlikely the cutting path is going to be linear, I do think the market is too aggressively priced against say a benchmark path of 25bps per meeting in Green.

UST curve saw little change last week (Purple to Green, change in Red) as the corrective selling came to a stall — longer-end marginally higher and short-end marginally lower. Assuming rate cut expectations are amply loaded into the short-end of the yield curve, I see risks of higher yields and a steeper curve through the persistence of a positive US data trend. Further, should policy easing expectations pare back, that should lift front-end yields and shift the yield curve higher.

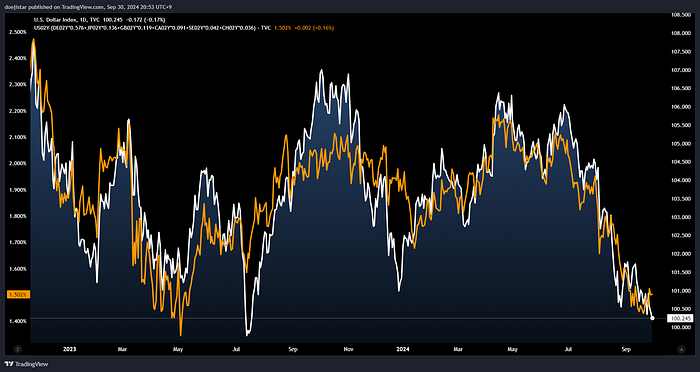

DXY is looking like a sick puppy… If you’ve been closly watching the USD trade in recent weeks, you may have had the thought the Dollar is still very unloved; you may have also observed that the Dollar selling isn’t getting very far as the days and weeks pass also. Against the DXY in white, I’ve plotted a simple DXY-weighted 2yr rate differential where we notice a slight divergence in the latter half of September. There is some concern that US election risks may cause the Dollar to fall out of favour, but given the relatively stronger US macro and carry, I think that will be enough to keep the Dollar resilient against some risk-aversion.

Trading views

Should be self-explanatory given the above analysis and comments:

- Short Equities

SPX mostly on top of longer-term NDX runners, China outperformance trade also appeals on short term momentum e.g. Long FXI/EFA - Long Energy, short Precious Metals

Continue to like trading around long Brent crude, and short Gold though Silver could be a better shout if risk-aversion builds ahead of elections. - Long USD vs JPY CHF EUR

No change to my preference for the higher yields and dollar theme. I would ask GBP to that list if risk turns more negative given positioning vulnerability and positive UK data momentum fizzling out.

That’s all for now — good luck trading!