2024.08.12 Weekly

Another brief one today just focusing on key developments around the recent sell-off and on going themes discussed over recent weeks.

Carry-unwind vs Recession

There is a lot of debate on whether the recent sell off in equities was the result of carry trades unwinding, or more about recession concerns. I’ve seen a good number of “carry had nothing to do with it” type of comments from many whose work and views I respect, but my feeling is that these comments mostly come from equities-focused traders, and less so from fx/rates traders who frequently witness such episodes of crowded funders getting squeezed and seeing huge unwinds.

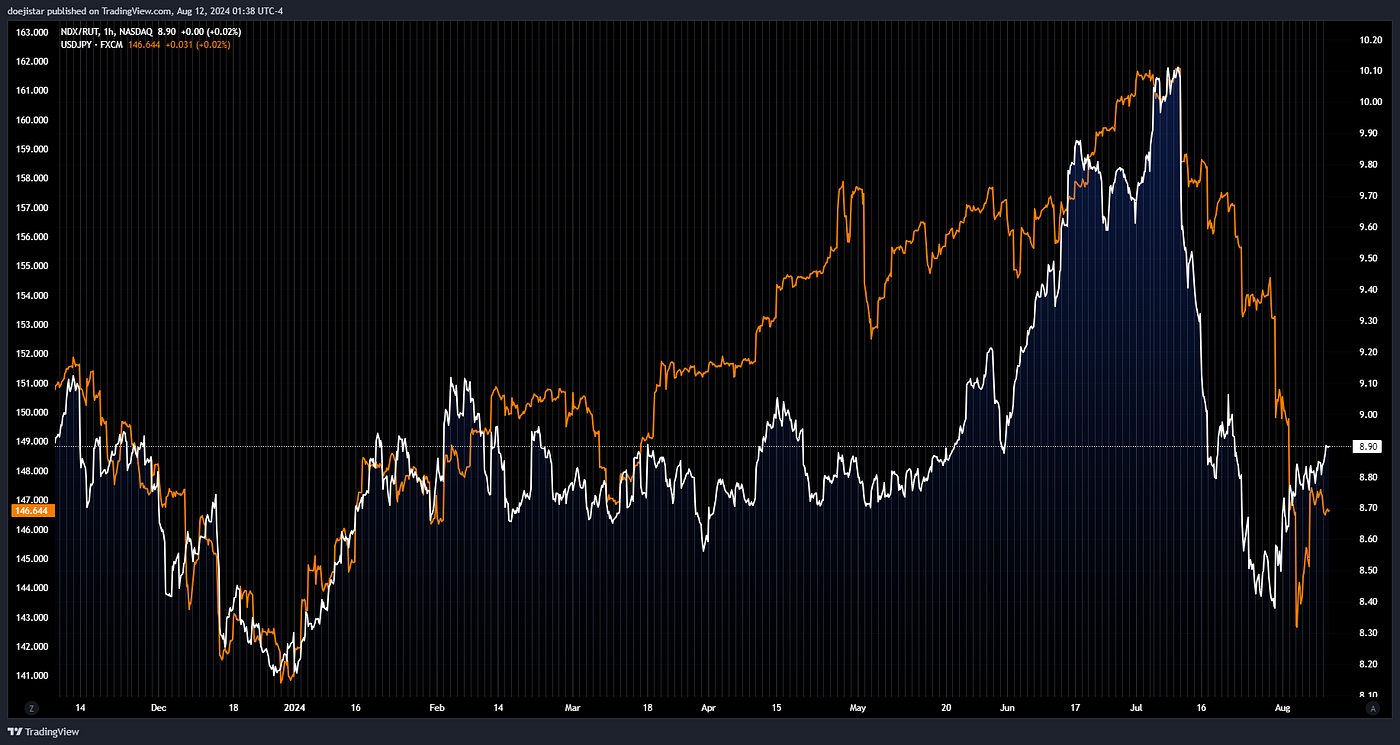

First, NQ vs USDJPY (Orange) chart which is at the centre of the ‘carry unwind’ debate. Further to the conventional carry trade being an interest rate arbitrage, the idea is that major funds have funded investments into tech stocks with cheap Japanese debt, such that if they unwind those leveraged investments, those flows would be reflected in USDJPY. Looking at what’s quite the epic chart — as it’s quite rare these move in lockstep, hard to argue that this is mere coincidence.

To make a point anecdotally, all I ever hear in Korea is people talking about investing in popular US tech stocks and that they prophetically expect them to continue rallying like it’s the second coming of Jesus.

Though not obvious as JPY, there has been moments USDKRW down-legs have coincided with NDX. I’d assume some of this cult-like sentiment in popular tech stocks exists in other developed countries as it does in Korea, to varying degrees. Thus not only is falling US front-end rates a key driver here, I think panic/margin selling of US assets from ex-US markets is also contributing to these fx unwinds.

Moving onto the recession narrative… NDX/RUT shows the selloff was well underway (beginning of July) before the recession narrative got any traction, and well ahead of the spike in volatility from a surprisingly big negative reaction to ISM manufacturing data (Aug1st) and NFP Unemployment rate (Aug2nd).

In fact, July saw solid S&P Services, core retail sales, a very strong GDP to reinforce the soft/no-landing narrative that initiated the sell-off in tech stocks and rotating into small-caps. This isn’t something you see when there is a genuine fear of a recession. Also interesting to note that USDJPY sold off alongside the tech sell-off at the end of last year — more evidence US tech positioning is heavily influenced by foreign inflows perhaps?

And if recession (oh no Sahm-rule triggered!) concerns were the driving narrative — whether correctly or not, then the ISM services report released the day after the Black-Monday sell-off looks to have set things right.

That report looks to have ended the sell-off with equities gapping up and continuing to recover for the rest of the week.

So, did carry really have nothing to do with the selloff?

Was recession concerns really the reason?

I’d probably say No to both and that carry unwind (if you’ll allow me to include extreme positioning, dispersion, and thematic concentration into this) was more the reason than recession concerns itself, and the latter simply accelerated it.

The aftermath

After an epic couple of weeks where 600–800 point daily ranges in NQ and 250pips in JPY has become the norm from the usual 250 points and 90pips, let’s take a look at how things have shaped up.

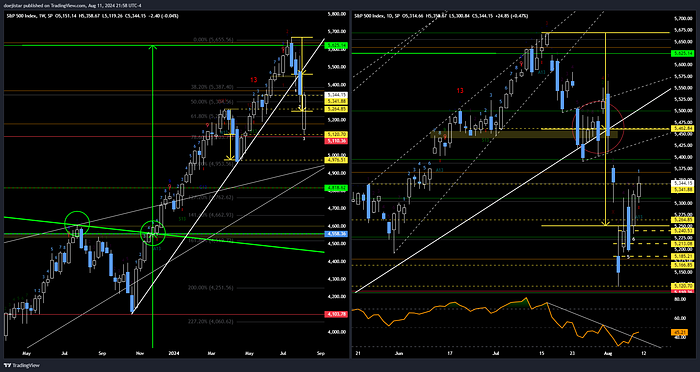

SPX saw a continuous recovery last week to finish well above the March swing high, above a major pivot area that coincides with the measured move of the recent breakdown, and Weekly RSI holding above the 50 mid-line and Daily RSI breaking out suggesting upside momentum has the potential to be healthy from here.

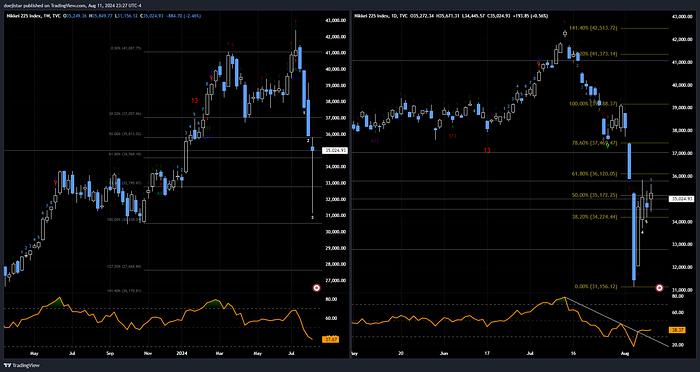

Japanese equities also one of the biggest hit in the recent selloff (which went as far as almost -27% from the July high within the space of a month!) retraced back to 50fib. It’s printed a massive Weekly bullish reversal bar, and with Japanese authorities panicking and giving reassurances to calm market volatility, it may be a good while till we revisit those levels below again.

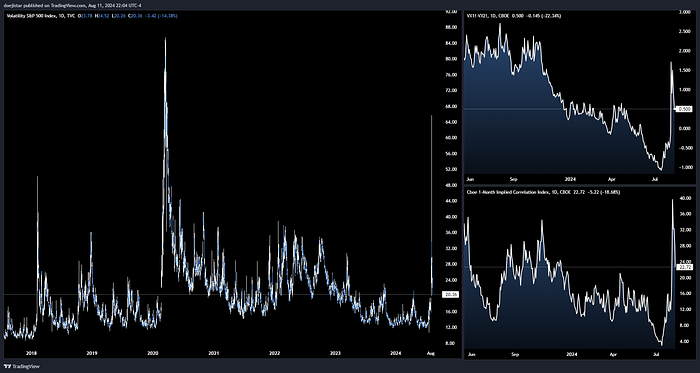

VIX reached its highest point since the Covid-crash and settled around the April peak where we had last seen a correction. Front month spread and implied correlation has pulled back alongside the bounce in equities, but it still remains elevated, at least relative to recent history.

With equities retracing back to the key pivot zone and 50fib, I think volatility indices will be key to whether the market has put in a durable bottom last week — i.e. we will need to see volatility continue to recede this week to gain confidence that a short-term bottom is in.

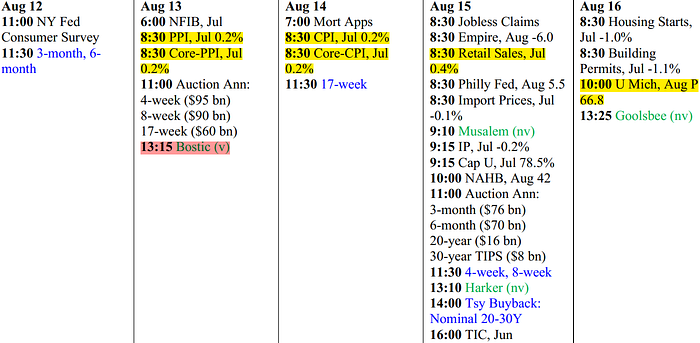

Looking ahead

Busy week… US Inflation and Retail sales the big ones:

US earnings season rolls on… nothing particularly stands out but China ADRs especially Alibaba could be particularly interesting to gauge China’s recovery, as with some US Consumer sector companies.

Elsewhere:

- UK employment and GDP

- New Zealand RBNZ decision

- Australia employment

- China Retail sales and Industrial production

Short-term trading views

Long NDX — how I like to express the rewind the unwind thesis. Personally I’m unsure about what the economic data is telling us — it’s very mixed. But while I do generally remain optimistic on the US economy, consensus appears to be building around economic slowdown concerns. I take my view from this that 1) initial rotation from tech stocks to small-caps could be premature, and 2) we see rotation back to quality (including major tech stocks) amid this macro uncertainty.

Long AUDJPY and AUDCHF— I continue to stay aggressively long AUD fading recession fears and oversold commodities. I think US rates will be giving back some gains and yields will inch higher as recession clouds clear thereby supporting cross-JPY pairs as well as cross-CHF.

Long AUDNZD — pro AUD and RBNZ cut trade:

I continue to have an interest in commodity longs but as I’m aggressively long risk in the above positions, I will not be taking positions in these though closely monitoring as it ties in with long AUD ideas.

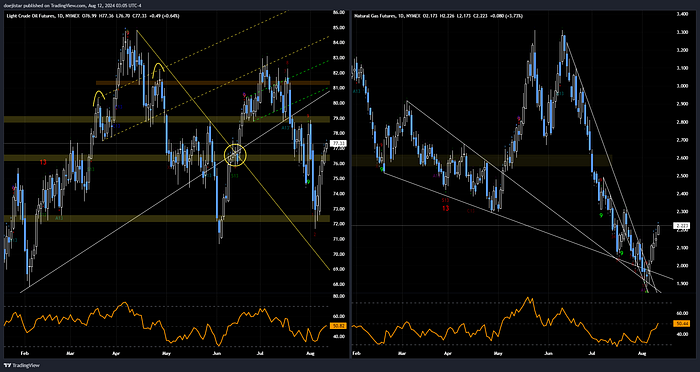

Crude and Natgas — Crude bounced from an important pivot level and recovering to what I’d consider a more reasonable range between 75–80. Natgas would be my choice if I took a position here for tactical reasons — technically more compelling, concerns of European gas supplies again, and while in a seasonally strong period where price can get bid up to ensure ample winter stores.

Copper and Silver — both are technically constructive after recent downtrends. Copper looked very extended below the 4 handle and looking positive above the handle after finding support at the trendline. Silver finding support at the April-May lows, and 161.80 downside extension. It’s carved out a wedge like structure and looks ready to breakout higher.

That’s all for now, have a great week trading!