2024.07.29 Weekly

I continue to lean tactically long to fade the deleveraging moves ahead of some mega-cap earnings this week. But I don’t plan to hang around for too long as we begin to enter a turbulent period for risk, and I do see risks of bond vol coming back if US data points to a bigger growth rebound (the reflexivity thesis I’ve been contemplating in recent weeks and months) and/or reduced potential for a September cut.

Many have commented on Tech longs being levered up via JPY as well as other currencies with foreign investors buying into popular tech stocks that has seen a big YTD-rally, thus leading to what looked like a carry unwind in currencies. This epic chart really could not be explained otherwise.

@RenMacLLC: Yen is overbought in a downtrend. Represents resetting of expectations and global liquidity flows…sold!

Further to the outsized move in JPY, there could be signs the dispersion unwind could be taking a breather, as I wrote on twitter last Friday: “Plenty claiming more deleveraging to come and could go on for weeks, but even if partially complete, I think this risk recovery is strong enough to stall that flow — less panic, pressure off margins and forced selling.” That ‘recovery’ hasn’t held as strongly as it looked like it may do as there seemed to be some residual selling late in the day and into close.

Even so, there are signs that buying activity has come back over the last two sessions with net buying volume equaling levels when SPX traded at the highs.

The VIX has also come off some ways since the pre-opening-bell Thursday high. Plenty of earnings and macro events to navigate, but barring any signficant surprises, I think relief is underway especially if index vol continues to come off and finishes the week in the low ‘teens.

Data review

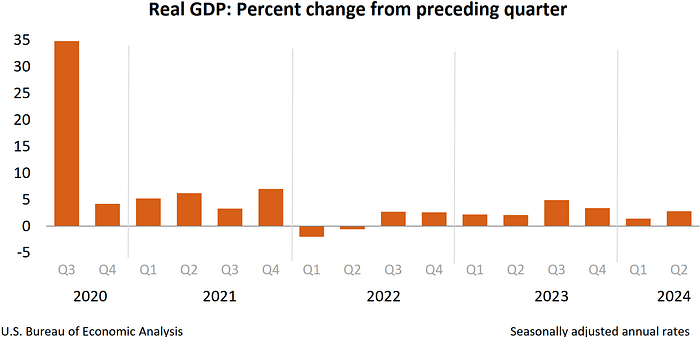

GDP advance estimate came in 80bps higher than expected at 2.8%, up from 1.4% in the 1st-quarter, largely owing to increased consumer spending — Consumption up 2.3% versus 2.0% expected. In nominal terms, annualised GDP growth was 5.2%, up from 4.5% in the 1st-quarter. These are strong numbers considering the GDP price index slowed to 2.3% from 3.1% in the 1st-quarter. BEA notes: “the acceleration in real GDP in the second quarter primarily reflected an upturn in private inventory investment and an acceleration in consumer spending. These movements were partly offset by a downturn in residential fixed investment.”

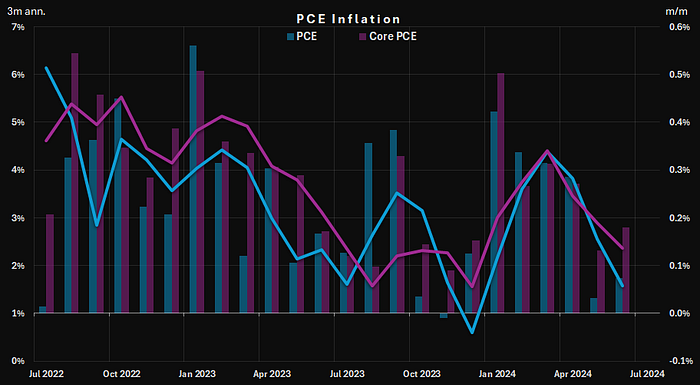

PCE prints was in-line with expectations which was rounded up from 0.07% and 0.18% for core. Inflation slowed back to the pace seen at the end of last year — on 3-month annualised basis, PCE is below 2% for the first time this year at 1.57% and core PCE at 2.36%, almost negating the 1st-quarter surge.

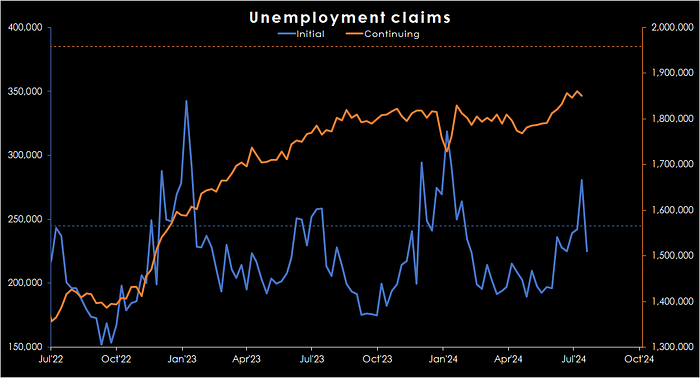

Initial claims saw a sharp drop back below the pre-pandemic 5-year average while Continuing claims has been steady so far this month after the big rise in June.

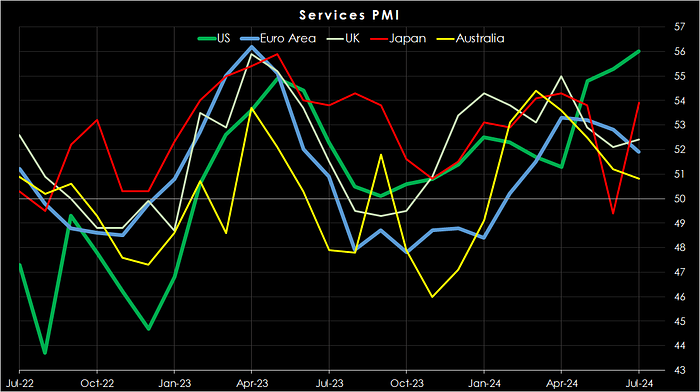

Last week’s S&P Flash PMIs continued to show the US dominating other major economies with Services continuing to accelerate faster at its strongest pace since March 2022:

Japan also saw a strong rebound in July led by services which saw activity growth hit a 3-month high.

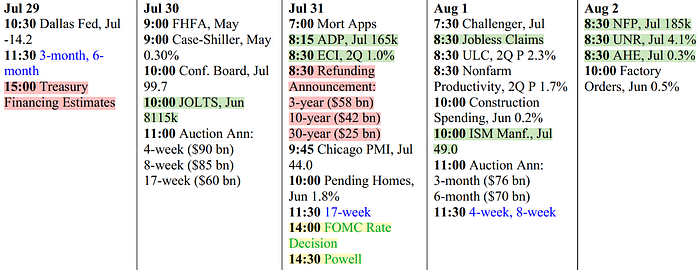

Busy week ahead

QRA estimates and composition is largely expected to be held steady with the same 3, 10 and 30yr auction sizes.

This week’s FOMC discussions is likely to move closer towards the first rate cut but I don’t expect any direct signalling from this meeting as they acknowledge progress on inflation, but stressing patience given data the persistence of strong data and uncertainty of upside risks while that remains the case.

Outside the US, major events include:

- TUE: German Preliminary CPI, Euro Area Flash GDP

- WED: BOJ, Australia CPI and Retail sales, Euro Area Flash HICP

- THU: BOE

- FRI: Swiss CPI

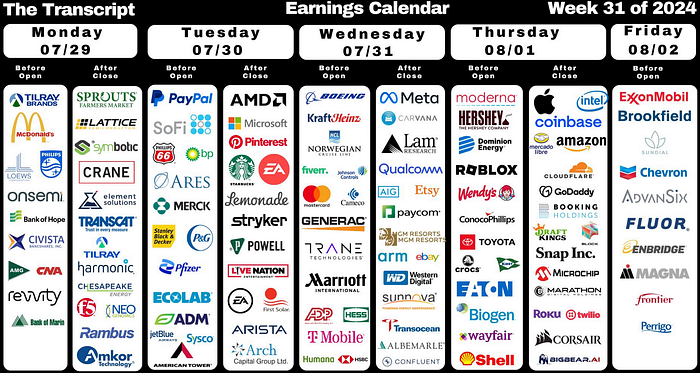

Also a very busy and important week of earnings with approximately 40% of SPX market cap reporting.

With top-line growth beginning to broadly fade, multiple expansion into year-end looks very challenging, so there will be a lot of focus on the big names to provide colour on the major narratives (e.g strong consumer spending and AI) and on how the SPX could trade into year-end.

NEWSFLOW

MARKETS

- US inflation data lifts global stocks, lowers Treasury yields (RTS). Wall St closes up on revival supported by inflation data, tech stocks — Indexes up on Friday: Dow 1.64%, S&P 1.11%, Nasdaq 1.03%; Indexes this week: Dow up 0.8%, S&P down 0.8%, Nasdaq down 2.1% (RTS). Europe’s STOXX 600 ends marginally higher on tech boost (RTS).

- Gold rises as yields slip after US data lifts rate-cut hopes — U.S. 10-year Treasury yields hit one-week low, Silver, platinum set for third straight weekly fall (RTS). Oil falls 1.5%, ends week lower on China demand fears (RTS). US oil/gas rig count rises in July in biggest monthly hike since Nov 2022 (RTS). Natural gas shows its staying power as US wind output slumps — Power producers in the United States are becoming increasingly reliant on natural gas for generation, even as the country builds out renewable energy capacity at a record pace (RTS), US wind power falls to 33-month low, generators burn more natgas (RTS). China’s rate cuts fail to revive iron ore and copper (RTS).

- Treasury likely to keep most auction sizes steady for now — likely to announce next week that it will keep most of its coupon-bearing Treasury auction sizes steady over the coming quarter, offering the market some relief after recent large increases. Additional expansions are expected down the road, however, as the U.S. fiscal trajectory worsens. “Treasury has strongly signaled that nominal auction sizes will not be increasing in the August-October quarter. The largest risk at this refunding would likely come from a strong change in the language that suggests coupon increases are coming sooner than we expect” (RTS).

AMERICAS

- Fed seen on track for September rate cut after good inflation data (RTS), June PCE index up 0.1% in June up 2.5% year-on-year, Core PCE price index gains 0.2% up 2.6% year-on-year, Consumer spending climbs 0.3%, income rises 0.2% (RTS). US economy regains speed in second quarter; price pressures easing — Second-quarter GDP increases at a 2.8% rate faster than 2% expected (RTS). US weekly jobless claims fall more than expected (RTS). US Home Prices Hit Record in June for Second Consecutive Month — Home sales slowed again, ending a disappointing spring selling season (WSJ).

- Bank of Canada cuts rates, sees weaker economy in 2024 — cuts key interest rate by 25 basis points to 4.5%, Trims 2024 GDP forecast to 1.2% from 1.5%, Central bank says future rate cuts to be data-dependent (RTS).

EUROPE

- First Bank of England rate cut since 2020 hangs on knife edge — Economists expect close vote at next week’s BoE meeting, Markets see 50% chance of a quarter-point rate cut, Inflation back at 2% target but set to rise again, Wage growth and services prices still too high for BoE (RTS), Bank of England plans expanded repo facilities to avert money market crunch (RTS). Some sun, football and promotions fuel UK groceries spending, says NIQ (RTS). Four years after pandemic shock, UK household saving stays high — ONS showed Britain’s households saved 11.1% of their income in the first three months of this year, up from 5.8% in the final quarter of 2019. This was the highest rate since 2010, excluding the start of the pandemic when it spiked to 27.4% (RTS).

- ECB’s Schnabel still sees tough ‘last mile’ in inflation fight — stuck to her cautious tone even as many of her colleagues were opening the door to more rate reductions (RTS). ECB likely to cut rates in September, former central banker says (RTS). Being boring key to central bank success says SNB’s Jordan — Jordan is due to step down at the end of September (RTS).

- German, French companies less hopeful over economic recovery — Germany’s stuck in a crisis — Ifo, Climate in French services worst since 2021 (RTS). Euro zone consumers stopped lowering inflation expectations in June (RTS). EU prepares two-step trade plan to tackle Donald Trump — If the Republican candidate returns to the White House, Brussels will offer a quick deal then threaten retaliation against tariffs (FT). Italy’s Giorgia Meloni pledges ‘relaunch’ of ties with China — Prime minister seeks to stabilise relations during visit to Beijing but also insists trade must be ‘more fair’ (FT). Trade links between UK and Germany stage post-Brexit recovery — Lift comes amid Prime Minister Keir Starmer’s bid to improve relationship with EU (FT).

ASIA

- China veers off beaten path with consumer stimulus — China repurposes some debt for consumer goods trade-in scheme, Move marks small shift in how Beijing thinks about stimulus, Programme limited in scale and marred by ‘inefficiencies’ -economists (RTS). China cuts several major interest rates to support fragile economy (RTS) — Chinese banks cut deposit rates to relieve squeezed margins (RTS), China lowers lending benchmarks after PBOC’s surprise LRP rate cut (RTS), PBOC surprises by lending again at lower MLF rates (RTS).

- Core inflation in Japan’s capital perks up, demand-driven price growth soft (RTS). BOJ to weigh rate hike next week, detail plan to halve bond buying, sources say — BOJ to taper bond buying gradually at pace near market consensus, July rate hike decision a close call, consumption outlook key, BOJ has ‘long way to go’ toward rate levels deemed neutral (RTS).

- Australian Flash PMI Falls to Six-Month Low; Price Pressures Still Evident (WSJ). New Zealand Consumer Confidence Jumps as Rate Cuts Appear on Horizon — The jump in confidence coincided with a hefty half-a-percent fall in inflation expectations (WSJ).

EQUITIES

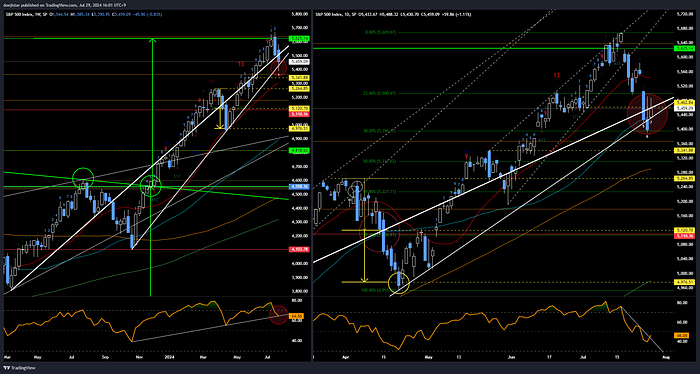

Technical structure on the global equities index remains weak despite showing tenative signs of pulling off a recovery. Ex-US found support at the 100dma and lower channel line with RSI turning higher — the stage is set for whether the market can sustain this bounce.

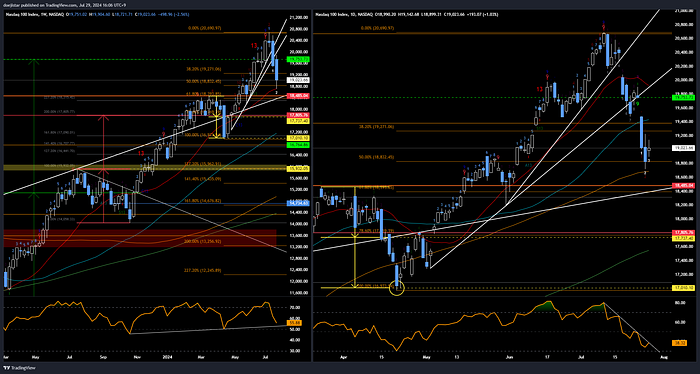

SPX has put in a bounce off the lower Weekly trendline whereas the Daily failed to close above 5460 which had it done so, would have made the bounce more technically robust. RSI is showing potential however with the Weekly support and Daily beginning to break higher.

NDX is less convincing but showing potential for an upside break after having found support at the 20wma and 50fib. A higher high and close would see the Daily RSI break higher.

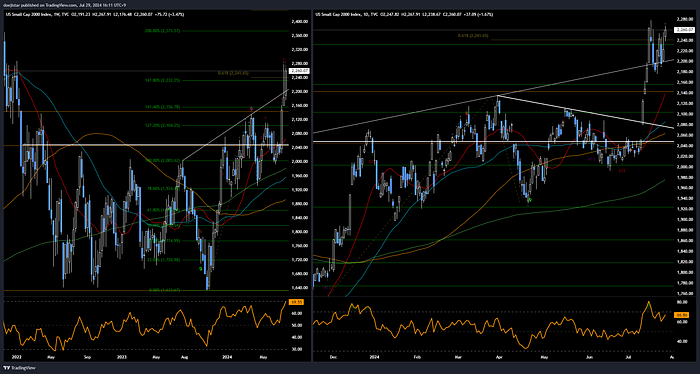

RUT small-caps rally is holding up well after a 15% rally off the June lows, but will it be more consolidation or a continued rip from here? With Weekly RSI just below the 70 mark and the highest reading since Dec’2020, some consolidation would be healthy at this juncture.

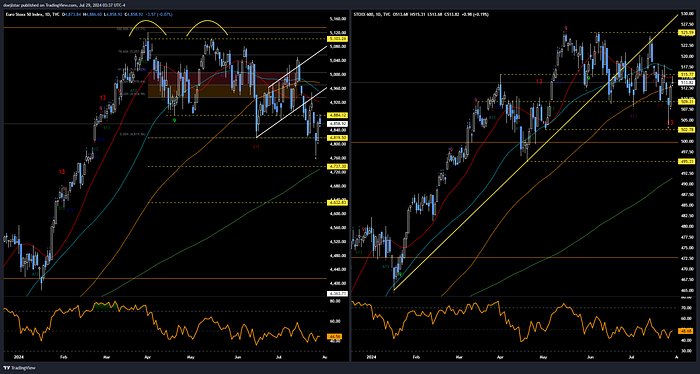

While US equities are showing some upside potential, European STOXX are showing limited potential with with RSI below the 50 mid-line, trend of lower highs and lows and the bounce capped by some key technical levels — Stoxx50 found resistance at prior neckline support, Stoxx600 capped by the 20dma.

Cyclical-defensive spread also telling a similar story of either sides potential. If it is to be believed that the market is in early to mid-cycle (i.e. rate cuts coming while growth is still strong and hard landing is avoided), then this pullback in the US spread could find a footing here.

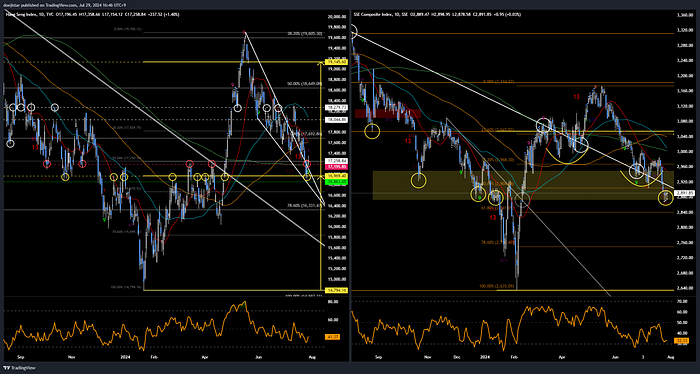

China equities slipped lower last week and I think these are great levels to bet on a bounceback — Hang Seng has bounced off a significant pivot level around the 17k handle with a Demark 9 countdown, and Shanghai composite reaching one of the last main supports below the 2900 handle and Feb’24 breakout level.

Nikkei and Kospi also looking a little more hopeful after the big pullback — the former showing a morning star formation with a demark 9 countdown that coincided with RSI nipping below the 30 level, and Kospi making a quick recovery back to a key pivot level after overshooting the 50fib to the downside with RSI breaking higher.

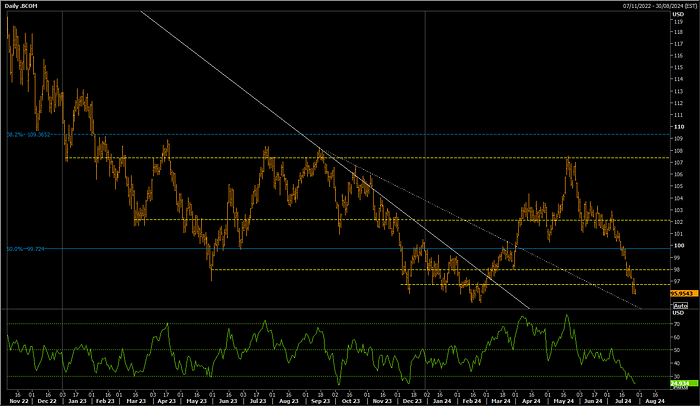

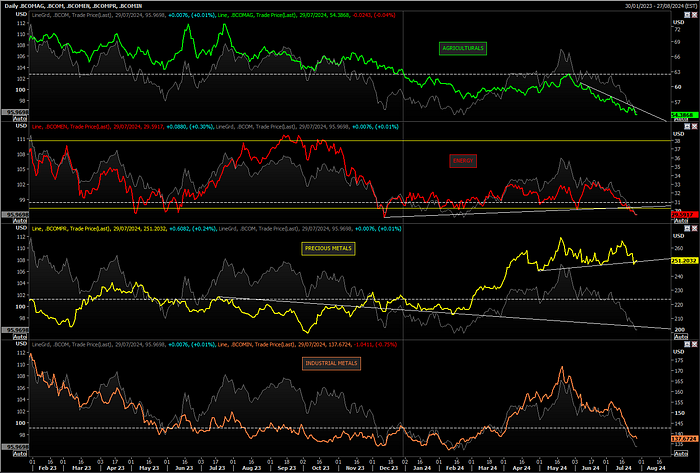

COMMODITIES

Bloomberg commodities index looks absolutely horrific. Should it though?

Agriculturals, Energy and Industrial metals — collectively making up over 2/3rds of the BCOM index, are all down for the year while Precious metals is the only sub-index of the above that is up. This picture is starting to look like fears of another global recession, a stark contrast to equity markets that is seeing a revival in small-caps and old-economy stocks.

China’s Dalian Iron ore futures has found support and should it continue to do so, it may signal the end of the extreme pessimism in commodity markets.

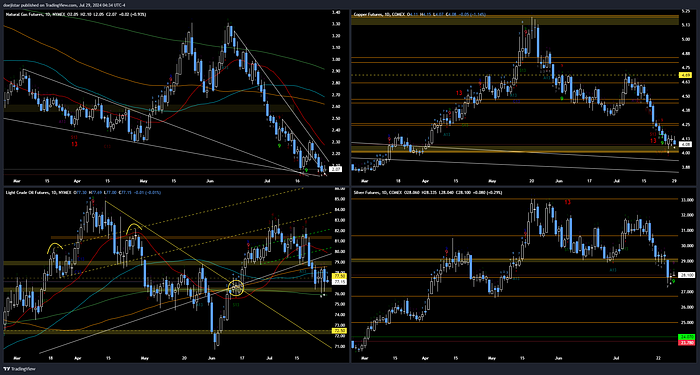

I’m keeping a close eye on these charts — Natgas is seeing some resurgent demand, Crude has been holding with resilience above the 200dma and June breakout level, Copper is eyeing 4 handle where I would expect some support, and Silver holding the 28handle with 9 countdown on print to start the week.

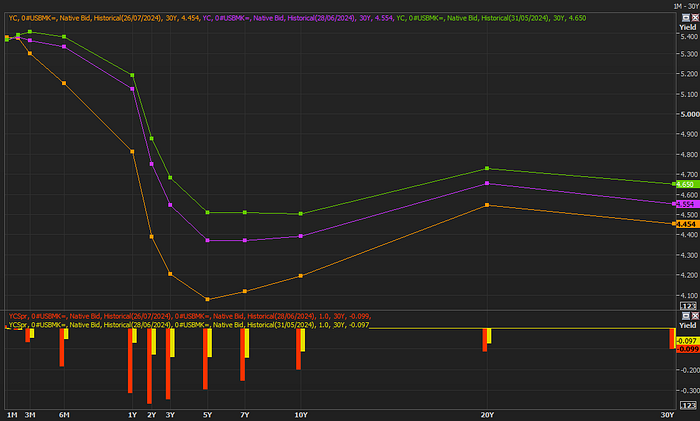

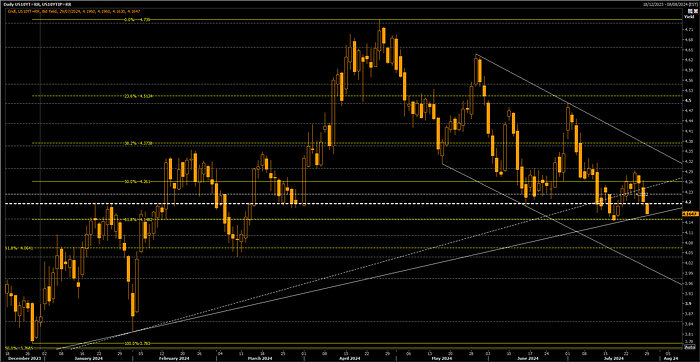

RATES

Bull steepening continued at a faster pace in July (Red) vs June (Yellow).

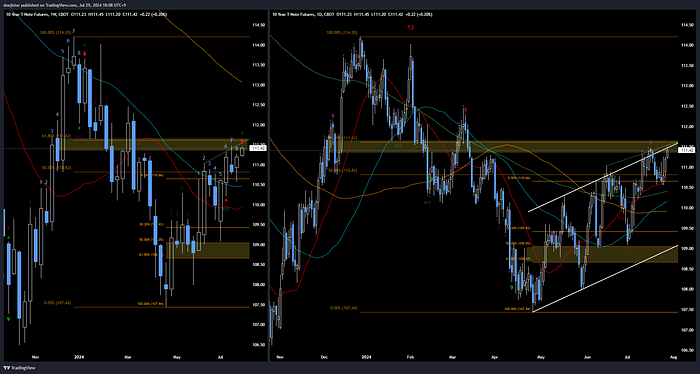

10yr continues to surprise me finishing lower on a day that has seen stronger economic data on multiple occassions. It has slipped below the 4.2% pivot and approaching an area of support around 4.15%.

Interestingly 10yr futures has a weekly 9 countup and upper daily channel resistance. This suggests it probably won’t take much (a bit of good data this week) for 10yr to trade down to recent lows around the 20dma and the 4.25% level.

CURRENCIES

- USD has been coiling up for a break higher and I think it could make that move this week given the technical observations on the US10yr pointing to upside risks to yields. A lot of data on deck this week could see USTs give up recent gains.

- EUR is looking increasingly toppy as we start the week. European PMI’s have been poor while the US continues to show strength. Had US yields not been slipping last week, I think EURUSD would have easily traded 1.08 already. I therefore see good potential for EURUSD heading back to 1.0750 should US yields rebound with plenty of potential triggers this week. I also think EUR would be a good funder for crosses such as EURAUD and EURNZD on the back of a potential relief rally in commodities.

- GBP enjoyed a solid rally on the back of political optimism. While I do think its due some reversion, I would prefer to look long on dips than chase it short. I think there is a good chance the BoE will not cave to the market’s dovish expectations with services inflation and wage growth proving sticky. Meanwhile, Starmer has impressed me with his foreign relations last year before becoming PM and I continue to think he will make a lot of progress on the UK trade front.

- CHF rallied back to the resistance level below the high (i.e. shoulder level) and with Swiss inflation this Friday, I’d be willing to bet on a solid NFP report and go long USDCHF this week with the chart already constructive for a bounce. AUDCHF long is also on the radar after printing a demark 9 countdown on Friday and should CPI and Retail sales come in strong.

- JPY ‘overbought in a downtrend’ as RenMac points out. Again, pointing to the observations on the US10yr and USD, I see potential for USDJPY reclaiming the 155–156 handles. AUDJPY is also technically attractive holding the 200dma and trendline starting from the Mar’23 low.

- In commodity dollars my preference has not changed — long AUD for pro-risk expressions, short NZD for bearish risk, mostly neutral but tactically long CAD as I see fit.

That’s all for now — good luck trading.