2024.07.08 Weekly

Reflexivity revisted

I’ve had a somewhat out-of-consensus view that we could see some ‘reflexive’ economic resilience from improving consumer and business sentiment in response to inflation coming down. There were some signs that could be case last month where we observed consumers still remained net positive on outlook while S&P Services PMI showed the fastest business activity acceleration in 26months.

But latest data failed to show any support to that idea with the US economic surprise index tumbling lower to start off July, and making the May rebound looking more like a blip. This has put me off my reflexivity thesis (lingering ‘upside risks’ that would keep the Fed well behind the curve for longer, seemingly overly pessimistic outlook, improved real incomes etc.) for the time being.

Further out, I still think that is a potential scenario that can come back into play if demand doesn’t crater. But as the current trend of data suggests, that scenario is looking far from immediate. Let’s review the data…

Data review

ISM’s reversed sharply with services back in contractionary territory.

ISM Services Business activity is at its weakest pace since the onset of the pandemic, New orders collapsed below the 50 line, Business inventory reflecting a weaker demand backdrop, and Employment remains in contraction.

NFP marginally beat estimates but more importantly, it is beginning to deviate lower from its longer run trend after the large downward revisions to the prior 2 months — 53% less than initially reported from 165 to 108k in April, 25% less from 272k to 218k in May. Big.

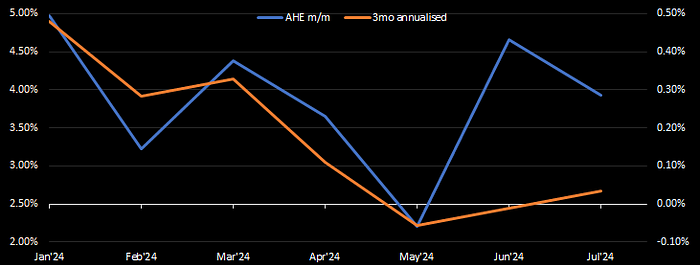

AHE came in as expected at 0.3% m/m which was 0.287% versus 0.432% the prior month unrounded. This puts 3month annualised wage growth at 2.67%, slowing considerably from around 4% at the beginning of the year.

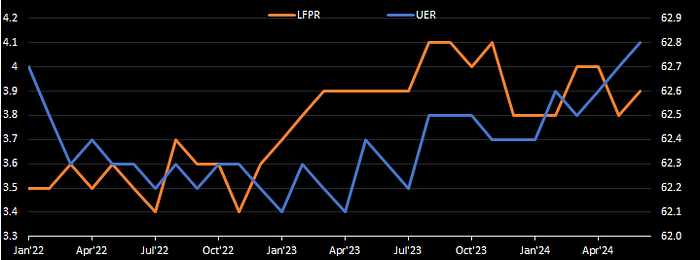

What seems to have got the most attention is the Unemployment rate reaching 4.1% in June, a rise of 3/10ths of a percent this year and to the highest level since November 2021.

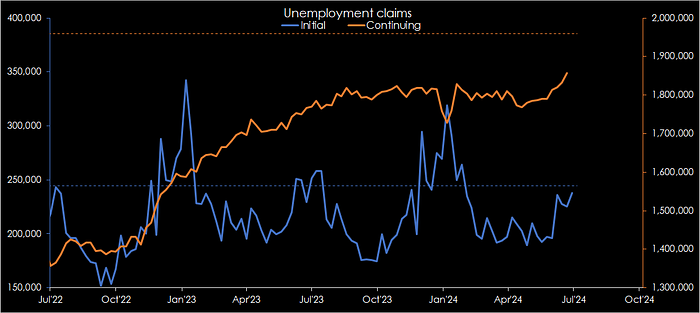

Initial claims was slightly below consensus while continuing claims was slightly above and rising for the 9th consecutive week. Still below the pre-pandemic 5yr average (dashed line), but should initial claims start to trend above that while continuing claims continues to rise, I’d begin to question whether the labour market is beginning to do more than just ‘moderate’ as that would be some indication that layoffs (via initial claims) and the ability to find reemployment (continuing claims) is worsening.

Looking ahead

Powell could come off dovish as he highlights recent data to show ‘progress, moderation, better balance’ and tells congress “See? I told you so” (that the reaccelerations in the earlier part of the year was likely a one-off). CPI PPI and UoM data will be a test to see whether the shift in markets pricing for earlier cuts is justified, and it probably will be given what the trends suggest.

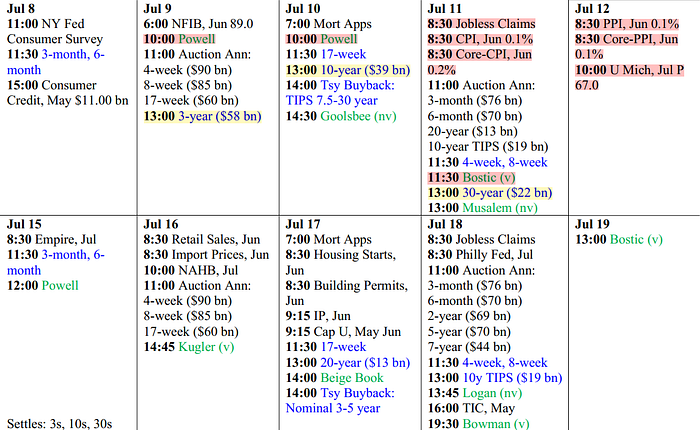

Plenty of UST supply coming in too — I expect a good 3 and 10yr auction but the 30yr could be interesting with curve steepening pressure to come back on the anticipation of Fed cuts and Trump getting his (probably inflationary) 2nd term. Not a lot else on the macro calendar — China CPI, RBNZ and UK GDP.

Q2 earnings season is about to get underway with the banks beginning to report on Friday.

SPX earnings expectations are even stronger for Q2 at 12.9%!

Expectations appear to be centred around improved cost control and overall profitability. Even so, that seems a high bar given what the macro data is telling us.

Russell2k small-cap expectations is also elevated, the movement of which looks closely linked to inflation and rate cut expectations — Q1 saw inflation rebound and rate cuts and earnings expectations pared back, Q2 saw inflation come back down and expectations turning more dovish again with earnings expectations improving.

Short-term momentum should stay positive given those expectations but for the short-term trader like myself, I see a lot of 2 way risks at this point and towards the end of the season as I sense the market may turn more tactical capitalising on those lofty expectations — 1) profit-taking from strong H1 gains, 2) slowing earnings growth risks ahead, 3) ‘more data for confidence’ Fed stance could be longer than assumed adding downside growth risks, 4) potential for softer guidance especially from a consumer angle though it could be offset by AI optimism, 4) avoidance of election risks. Such a scenario would align nicely with strong Q3 seasonal trends which I could see play out.

NEWSFLOW

MARKETS

- S&P 500, Nasdaq post record closes Friday as jobs report raises Fed rate cut hopes (CNBC). Japanese stocks gain biggest weekly foreign inflow in 2–1/2 months (RTS). Asian stocks draw robust foreign inflows on US rate outlook, tech rally (RTS).

- Tesla shares wipe out loss for the year with 27% rally this week (CNBC), best 8-day performance in nearly 3 years (MW). Earnings Season to Test Investors’ Faith in Big Tech Stocks —Wall Street’s upbeat earnings expectations set high bar for US companies (FT), S&P 500 companies are expected to report the biggest quarterly profit jump since early 2022 (WSJ). US consumer goods companies are losing upper hand on pricing (FT).

- Case for September Rate Cut Builds After Slower Jobs Data — Jobs report shows the unemployment rate ticked up to 4.1%, indicating slack in what has been a strong labor market (WSJ). Powell says Fed has made ‘quite a bit of progress’ on inflation but needs more confidence before cutting (CNBC), Minutes of June meeting showed some officials were concerned about effect of high rates on job market (FT).

- Treasuries Snap Losing Streak Amid Signs US Economy Is Slowing — Five-year note yields slide as much as 10 basis points, Swaps traders still expect two Fed rate cuts by year-end (BBG). Bond market re-focus on US elections throws wrench into 2024 rally hopes (RTS). Twitchy, Truss-scarred UK bond market awaits a Labour government (RTS). Rising Government Debt Threatens Financial Stability, Inflation, BIS Says — warned rising debt levels exposed governments to risk of a crisis similar to that which roiled the UK in 2022 (WSJ). Crushing Debts Await Europe’s New Leaders — Planned largess by election winners in Britain and France is on a collision course with soaring debts and deficits (WSJ). Jay Powell says US needs to cut deficit ‘sooner rather than later’ (FT).

AMERICAS

- US economy added 206,000 jobs in June, unemployment rate rises to 4.1% — better than the 200,000 forecast though less than the downwardly revised gain of 218,000 in May, unemployment rate unexpectedly climbed to 4.1%, tied for the highest level since October 2021, Average hourly earnings increased 0.3% for the month and 3.9% from a year ago, both in line with estimates (CNBC). ADP Private payrolls grew by just 150,000 in June — less than 160,000 expected and below the upwardly revised 157,000 in May, The pace of wage gains also moved lower for those who stayed in their jobs, down to 4.9% on a year-over-year basis for the smallest increase since August 2021 (CNBC). US Services Activity Contracts at Fastest Pace in Four Years — ISM index of services slumped 5 points in June to 48.8, Measure of business activity also weakest since May 2020 (BBG). US manufacturing extends slump; inflation pressures ebbing — ISM Manufacturing falls to 48.5 in June from 48.7, New orders employment and production measures contract,

Price paid for inputs measure lowest in six months (RTS). US construction spending unexpectedly falls in May — dipped 0.1% after an upwardly revised 0.3% increase in April (RTS). - Donald Trump distances himself from right-wing ‘Project 2025’ policy blueprint — Conservative groups have outlined far-reaching overhaul of federal government should ex-president clinch second term (FT). Biden is convinced he can win. Democrats say prove it (Politico).

- Canada’s rising jobless rate pushes case for July rate cut — Jobless rate at 29-month high of 6.4%, Youth unemployment at decade high except pandemic years, Canada lost a net 1,400 jobs in June (RTS). Canada’s services PMI falls to three-month low in June — headline business activity index fell to 47.1 from 51.1 in May (RTS). Canada posts third straight monthly trade deficit in May — Exports, barring the U.S., post record fall, Exports drop by 2.6%, giving back gains of April (RTS).

EUROPE

- Keir Starmer begins tour of UK nations to ‘reset’ relations (FT). UK shop prices fall in June as cost of living crisis eases (FT), UK shop price inflation weakest since October 2021, retailers say (RTS). UK house prices edge down in June — Property prices fell by 0.2% last month from May and over the 12 months to June they rose by 1.6%, Halifax said. “This continued stability in house prices — rising by just +0.4% so far this year — reflects a market that remains subdued, though overall activity has been recovering” (RTS). UK construction growth cools ahead of election — Construction PMI fell to 52.2 in June from 54.7 in May, below the median forecast of 53.6 (RTS).

- Services Inflation Stays Strong in Eurozone, Complicating Rate-Cut Policy — Consumer prices were 2.5% higher in June than a year earlier across the 20 nations that share the euro (WSJ). German industrial orders unexpectedly fall in May (RTS). Euro zone factory activity decline deepens in June, PMI shows (RTS). ECB minutes reveal doubts over rate cut — Move to lower borrowing costs concerned many policymakers as inflation and wages moved in opposite direction (FT).

- Left leads French election, Le Pen’s far right party third-placed — France was on course for a hung parliament in Sunday’s election, with a leftist alliance unexpectedly taking the top spot ahead of the far right, in a major upset that was set to bar Marine Le Pen’s National Rally (RN) from running the government (RTS). European central bankers warn of risks to region’s economy — ECB policymakers view French elections as sign of a broader shift in a more populist, protectionist and turbulent direction (FT).

ASIA

- China’s June factory activity contracts again, services slows — NBS PMI was at 49.5 in June unchanged from May and in line with median forecast of 49.5, while sub-index of production was above 50 in June, other indexes of new orders, raw material stocks, employment, supplier delivery times and new export orders were all in contractionary territory; services PMI sank to 50.2 a five-month low, construction PMI slipped to 52.3 the weakest reading since July last year (RTS). Chinese factory activity up among smaller firms amid broader slowdown — Caixin Manufacturing PMI rose to 51.8 in June from 51.7 in the previous month, marking the fastest clip since May 2021 and surpassing analysts’ forecasts of 51.2, activity among smaller Chinese manufacturers grew at the fastest pace since 2021 thanks to overseas orders ,even as a broader survey indicated weak domestic demand and trade frictions had led to another industrial sector contraction (RTS). Japan June factory activity unchanged amid higher costs — final au Jibun Bank manufacturing PMI was at 50.0 after a brief improvement to 50.4 in May (RTS). South Korea factory activity sees fastest growth in 26 months on rising demand — manufacturing PMI rose to 52.0 in June, from 51.6 in May (RTS).

- Japan’s GDP downgrade, shaky business mood cloud BOJ hike timing — Big manufacturers’ sentiment index at +13 vs +11 in March, Service-sector index at +33 vs +34 in March, Corporate inflation expectations rise slightly, Sharp downgrade to Q1 GDP seen affecting BOJ’s forecasts (RTS). Japan household spending falls unexpectedly, clouds BOJ rate path — May household spending falls 1.8% yr/yr vs forecast +0.1%, Analysts expect rebound in Q2, divided on rate hike timing, Data likely to affect BOJ’s forecast and July rate decision, BOJ to highlight broadening wage hike in report, sources say (RTS).

- South Korea June exports rise for ninth month but miss forecasts (RTS). South Korea inflation hits 11-month low as supply pressures ease (RTS). Australia job ads fall 2.2% in June, ANZ-Indeed data shows (RTS).

EQUITIES

All countries world index is showing some interesting signals with price getting finely wedged-in as it pushes ATHs. Technically, this is a structure that warrants a high degree of caution.

Developed and Emerging market indices both look very strong but there is a smidge of uncertainty here technically with the negative divergences and key levels left to be tested this week.

SPX is very close to completing its breakout objective meeting the 161.8 fib extension where I’d expect some reaction. There is also Weekly 9 countup printed last week but needs to be taken with a pinch of salt without price action complimenting the count. The Daily however is on a 7 countup, likely to reach 9 on the Tuesday close, and where it could meet the tehcnical objective levels around 5625–40.

NDX is basically the same as above with one difference, Daily countup is on a 6 and would reach 9 on the Wednesday close, a day after SPX.

NYFANG index tends to observe trendlines well with firm price tests and pivots. Last week’s weekly bar has shot up using the upper rising wedge line as the base after a few weeks of indecision there. RSI is in the extremes as with other US index charts above and on course to print a 9 countup on Tuesday close.

European equities still looks like its on fumes. I’ve been in and out of short Stoxx50 a couple times but still rather unconvinced on the upside due high government debt and spending being a key issue, even though the conclusion of the French elections providing some reprieve. Technically, there is a potential shouldering developing and I will wait to see how it develops as US rate cuts and lower dollar is likely to give risk a lift than not for the time being, as well as the other charts above hinting caution.

Asia starts the week on the backfoot today and frankly I expected a stronger start given the case for US rate cuts building again is likely to take some pressure off the USD. Nonetheless, uptrend in Japan and Korean indices looks in-tact, while China equities are pulling back to a key technical region where it could find renewed buying power.

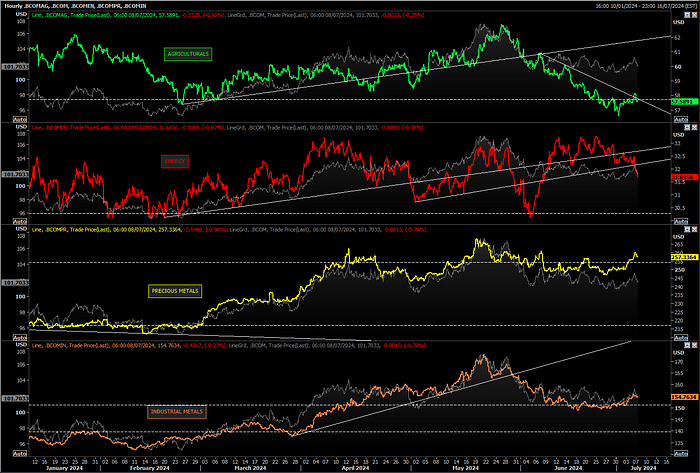

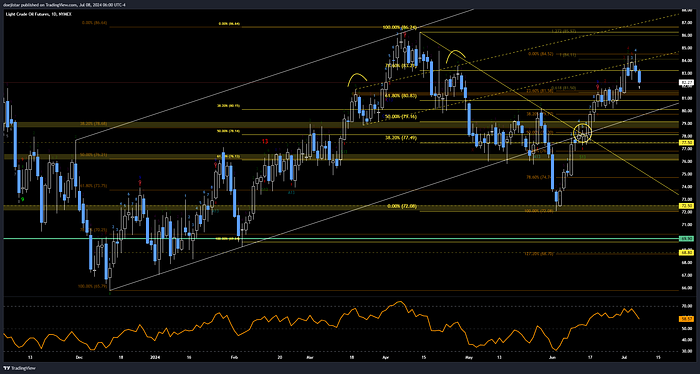

COMMODITIES

Aside Energy, it was a good week for commodities and looks set to recapture the uptrend if the USD continues to ease.

Recent uptrend in Crude and Gasoline prices looks to have buckled and likely to make its natural 38.2–50 retracements of the recent rally.

I look for CL to make a it’s way back to recent support and 20dma just above the 80 hanlde and 38.2 fib just below. If it continues to stay heavy into that area and global economic data continues to underwhem, I think 78–77.5 is on the cards.

RATES

Big move lower in yields with the belly 3s 5s 7s almost 30bps lower since the end of May (Green). Economic data continues to come in on the softside of expectations and could see another 10bps drop this week on a CPI miss. I also expect decent demand for auctions this week and see risks skewed toward more downside.

10yr started at 4.35% and traded as low as 4.269% breaking below the most recent trendline. I don’t expect it to go much higher than where it is currently — hovering above 4.3% and expect it to drift towards 4.2% assuming another soft CPI print this week e.g. a flat to 0.1% m/m print. That should increase the odds of a September cut some more of which I’m only just beginning to start leaning towards, and I do think a cut on August 1st FOMC is still one CPI print too soon for them to be moving with any ‘confidence’.

CURRENCIES

A lot of conflicting signals above both fundamentally and technically (e.g. growth slowdowns vs earlier fed cuts, strong price action vs cautionary signals), so my intention is be nimble in general. With that, these are the FX themes I look to trade around on a short-term basis.

- USD mildly negative — with US slowdown and cuts dominating the narrative, I like USDJPY and USDMXN downside, going for the rate sensitve pairs.

- GBP positive, EUR negative — UK data is looking less bad as the weeks go by and Starmer is likely to continue shaping a positive outlook for UK trade. Europe has the trickier so-called ‘last-mile’ in my view — sticky services inflation amid high debt spending and slowing activity that could soon send the composite PMI measure into contraction territory: “demand conditions were a restrictive factor for eurozone businesses at the end of the second quarter; total new workloads shrinking for the first time since February; decrease in overall sales reflected a steep drop in manufacturing new orders, services demand increased at a weaker rate; decrease in new export business outstripped that seen for total new orders, implying a stronger drag on demand from external sources rather than domestic”. I expect GBPUSD to continue showing upside resilience while EURUSD upside to stay limited, EURGBP to stay under pressure.

- AUD positive vs NZD negative — stark fundamental differences with the AUD economy being more resilient, still battling some inflation pressures, and potential crosswinds from an albeit gradual China recovery. New Zealand on the other hand is going through a major slump, empty shops, services in contraction for 3 straight months with the pace quickening, and rapid disinflation. I like AUDNZD GBPNZD longs, and depending on which way risk is blowing AUDUSD long NZDUSD short.

Good luck trading!