2024.04.08 Weekly

Big focus on CPI this week, then earnings for the rest of the month to see whether Equities can continue to push new highs for the April seasonality to play out. We’ve had some strong labour market data last week which I review below, and if this week’s CPI beats to bring back some renewed selling pressure in rates, that would provide some confidence that Equities have entered a corrective phase (or a consolidative at the very least) for the near-term. In the meantime, I still see risks of higher US yields and widening differentials in favour USD to keep posing questions to the risk rally and continue to maintain a tactically bearish risk view.

Labour data review

Some conflicting signals from the labour market data with another strong NFP report — almost a 100k more than expected and 33k higher than the previous month’s gain.

Strong job gains is at odds with the declining trend in Job vacancies to gradually rising Unemployment numbers — reflecting the softening hiring intentions seen in regional and ISM surveys. ISM employment component has been in contraction since the 50.5 print in January for Services while manufacturing has been contraction for the last 6months.

But so far, we are so not seeing the Beveridge curve effect of labour market loosening putting downward pressure on wages which is picking up again in recent quarters. AHE remains around the 4.5% and the ADP report also highlights a particularly strong rebound in yr/yr pay for Job changers, which doesn’t quite support the idea that the labour market and wage pressures is easing meaningfully. The Employment Cost Index should be interesting at the end of the month…

CPI upside risks?

The key macro event this week will be the US CPI on Wednesday — expected to print 0.3% m/m for both headline and core which is inline with the Cleveland Fed inflation nowcast:

M/m headline and core prints last month was at 0.4%, so an inline print is likely to be welcomed by markets that inflation is still on the right track. There could be a rounding-up risk to the headline number with Energy (Gasoline prices up 7.55%) and Food (BBG Agricultural index up 2.51% up last month) commodities continuing its ytd-rally, as well as the cost ofs fast-food and eating out continuing to climb according to media reports.

Further, while prices paid components have been slowing for services over the last quarter, they still remain in expansion, and manufacturing prices have continued to accelerate since 45.2 in November to 55.8 last month. Also some media reports has pointed to some fresh supply chain disruptions over the last month. Are these realistic upside risks to the March inflation report? We shall see…

11% earnings growth?

A few weeks ago, I noted that forward earnings expectations were easing off and plateuing. It’s ramped up again over the past month ahead of earnings season to back where we were at the beginning of the last Q4 earnings season. I still suspect that we are, at the very most, plateuing at these growth rates and I think this sets a high bar for Q1 results to maintain.

“If we’re going to continue to make significant gains in the stock market, we have to not just meet, but probably exceed those earnings estimates”

— BMO Wealth Management CIO (RTS).

As covered last week, April is a seasonally strong month for Equities and I suspect that seasonal pattern is a reflection of a strong period for corporate profits at the turn of the year with earnings results released throughout the month. So beyond the CPI print, I still reserve some time to assess whether earnings growth is decelerating enough to maintain the view that equities will need to blow off some steam.

NEWSFLOW

MARKETS

- Traders Favor Two Fed Cuts in 2024 as Treasury Yields Near 4.5% (BBG). Doubts Creep In About a Fed Rate Cut This Year — Traders started the year predicting up to seven rate cuts. Now, many are betting on one or two — or none (WSJ). PIMCO trims 2024 Fed rate cut expectations to 2 after jobs report (RTS). Powell Says Fed Has Time to Assess Data Before Deciding to Cut — Too soon to say whether recent price pickup more than a bump, Recent data have not materially changed overall picture (BBG). ‘Upside’ inflation risks keep Fed officials wary of turn to rate cuts — Bowman: “we are still not yet at the point where it is appropriate to lower the policy rate, continue to see a number of upside risks to inflation, While it is not my baseline outlook I continue to see the risk that at a future meeting we may need to increase the policy rate further should progress on inflation stall or even reverse, it will eventually become appropriate to gradually lower the federal funds rate to prevent monetary policy from becoming overly restrictive”; Logan: “ much too soon to think about cutting interest rates, need to see more of the uncertainty resolved about which economic path we’re on” (RTS); Mester: “It’s hard for me to get there by May, I think three is still reasonable, but it’s a close call”, raised estimate of the longer-run federal funds rate from 2.5% to 3%; Daly: three cuts remained “a very reasonable baseline” (FT); Kashkari: “In March I had jotted down two rate cuts this year if inflation continues to fall back towards our 2% target, If we continue to see inflation moving sideways, then that would make me question whether we needed to do those rate cuts at all” (BBG); Bostic: expects one rate cut this year in the 4th Quarter (BBG). Summers Says Hot Jobs Data Show Neutral Fed Rate ‘Much Higher’ (BBG).

- Middle East tensions spook markets (RTS). Cyclicals drive modest gains across European stocks (RTS). UK stocks climb on boost from auto, mining stocks after upbeat data (RTS). Earnings Season to Test Stock-Market Rally — Wall Street expects S&P 500 companies to report a third straight quarter of profit growth (WSJ). US stocks’ lofty valuations in spotlight as earnings season nears — “If we’re going to continue to make significant gains in the stock market, we have to not just meet, but probably exceed those earnings estimates” BMO Wealth Management CIO (RTS). Rising Treasury yields pose a test for richly valued US stocks (RTS). The fading ex-Mag7 earnings outlook — “Broadening out” is the hot new US stock market narrative, with the equal-weighted S&P 500 index actually beating its top-heavy conventional counterpart over the past month (FT). First-quarter flows to tech stocks third largest on record — BofA (RTS). Global equity funds see outflows amid uncertainty over rate cut timing (RTS). Foreign inflows in Asian stocks surge in March on rate cut prospects, China data (RTS). Global supply of equities shrinks at fastest pace in decades — Uncertain executives are favouring share buybacks over tapping buoyant markets to fund investment (FT).

- El-Erian Sees US Exceptionalism at Play Again With Job Growth Soaring (BBG). US dollar to stay strong as markets delay Fed rate-cut bets: Reuters poll (RTS). ECB continues to lay groundwork for June interest rate cut, March accounts show (RTS). Long Shadow of Fed to Fall on ECB After Lagarde’s First Cut (BBG). Japan warns against excessive yen moves, repeats verbal intervention — PM Kishida says excessive yen volatilty undesirable, repeats FX warnings of finance minister Shunichi (RTS). Japan won’t intervene unless yen slides below 155, says ex-FX diplomat Watanabe (RTS). Bets Against Yen at Highest in 17 Years as Test of 152 Looms (BBG). China Maintains Yuan Defense After Currency Nears Red Line (BBG). Reserve Bank of New Zealand to cut rates in Q3 but may wait longer: Reuters poll (RTS). Tame Swiss inflation opens door for more SNB rate cuts, weighs on franc (RTS).

- Oil’s Under-the-Hood Signals Tell Tale of Bullish Market — Options, timespreads, fund flows are positive as crude gains (BBG). OPEC+ keeps output policy steady as oil nears $90 a barrel (RTS). Russia fulfils its OPEC+ oil commitments in full, Novak says (RTS). OPEC+ gets oil price to its sweet spot, the trick is keeping it there (RTS). BofA hikes 2024 oil forecasts on tighter supply, geopolitical risks (RTS). US oil and gas output was severely hit by winter storm (RTS). US drillers cut oil and gas rigs for third week in a row — Baker Hughs (RTS). US manufacturers emerge from slump, set to boost fuel use (RTS).

- Gold shatters new records as Mideast tensions add to bullish mix (RTS). Gold bulls eye more record highs despite lightning gains (RTS). Cocoa Falls as Rally Loses Steam and Farmers Get Pay Hikes (BBG). Robusta Coffee Hits Fresh Record as Dry Weather Risks Next Crop (BBG). Arabica Coffee Surges to Highest Since 2022 on Short Covering (BBG). Bird flu hits Texas dairy cows, hens, human as ducks migrate (RTS). Bird flu dairy cow outbreak widens in Ohio, Kansas, New Mexico (RTS). Wider bird flu spread raises concern for humans, animal health body says (RTS). Food inflation across rich nations drops to pre-Ukraine war levels — Annual change in prices across 38 industrialised countries eased to 5.3% in February, says OECD data (FT). World food prices rebound from three-year low, says UN agency (RTS). Panama Canal drought could threaten supply chain, S&P says (RTS).

US

- Strong US labor market underpins economy in first quarter — NFP increase 303,000 in March, Unemployment rate falls to 3.8% from 3.9%, Average hourly earnings rise 0.3% up 4.1% year-on-year (RTS). US Companies Added 184,000 Jobs in March, ADP Data Show (BBG). US job openings rise slightly; labor market steadily easing — Job openings increase 8,000 to 8.756 million in February, Job openings to unemployment ratio falls to 1.36 from 1.43, Quits rate unchanged at 2.2%; layoffs rate rises to 1.1% (RTS). US service sector expands moderately in March; price pressures easing — ISM non-manufacturing PMI fell to 51.4 from 52.6 in February. It was the second straight monthly decline in the index since rebounding in January, new orders slipped to 54.4 from 56.1, business activity edging up to 57.4 from 57.2, prices paid for inputs dropped to 53.4 from 58.6 the lowest reading since March 2020 (RTS). US manufacturing on the mend; rising raw material prices pose obstacle — Manufacturing PMI jumps 2.5 points to 50.3 in March, prices paid rose to 55.8 from 52.5, New orders and production measures rebound, Construction spending drops 0.3% in February (RTS). US Consumer Borrowing Rises, Driven by Credit-Card Balances — largest increase in credit-card balances in three months (BBG). Business Bankruptcies Jump as Slow Wave of Failure Speeds Up — Commercial insolvencies jumped 43% in the first three months of 2024 (BBG). Trump’s Rallies Are Losing Their Luster as a Key Campaign Tool — as Trump still lags behind President Joe Biden in campaign cash, the rallies are losing their money-raising power as well (BBG).

- Canada Unexpectedly Sheds Jobs, Unemployment Rises to 6.1% — Accommodation, food service, wholesale, retail lead job losses (BBG). Canada services PMI falls in March as downturn lengthens (RTS). Canada launches $6 bln housing fund in bid to quell housing crisis (RTS). Trudeau Unveils $1.8 Billion Package for Canada’s AI Sector (BBG).

EUROPE

- Eurozone inflation falls to 2.4% in March — Lower than expected figure bolsters expectations of ECB interest rate cuts by summer (FT). Inflation down in German states, pointing to national decline (RTS). Euro-Zone Companies Expect Wage Growth to Moderate, ECB Says (BBG). Weak rise in orders points to more gloom for German industry (RTS). Euro zone factory downturn deepened in March but some recovery signs, PMI shows (RTS).

- UK wage growth expectations fall to 2-year low — Bank of England survey of businesses will ease rate-setters’ concerns over stickiness of inflation (FT). UK recruiters report slowest growth in starting pay in over 3 years (RTS). UK shop price inflation drops below 2% for first time in 2 years (FT). UK construction sector ekes out first growth since August 2023, PMI shows (RTS). UK house prices fall for first time in 6 months as rates stay high (RTS). Large UK companies see lowest uncertainty in nearly 3 years (RTS).

ASIA

- China’s forecast-beating economic data buys officials time to figure out fix (RTS). China’s services activity growth speeds up in March, Caixin PMI shows (RTS). China’s factory activity expands at fastest clip in 13 months, Caixin PMI shows (RTS). China’s new home prices rise at fastest pace in over 2–1/2 years, survey shows (RTS). China’s Shimao faces liquidation suit over failure to pay $202 million loan (RTS).

- South Korea factory activity contracts in March as weak domestic demand drags, PMI shows (RTS). Japan’s March factory activity shrinks at slower pace, PMI shows (RTS).

- Japan real wages fall for 23rd straight month in February (RTS). Japan’s economy recovers to full capacity, keeps alive BOJ rate hike prospects (RTS). Japan’s service sector mood climbs to 33-yr high, leaves scope for more BOJ hikes (RTS). Bank of Japan hints at near-term rate hike, pushing yields higher — Ueda said inflation would likely accelerate from “summer towards autumn” as bumper pay hikes push up prices. (RTS).

EQUITIES

Global equities put in the first week of meaningful selling for the first time since the first week of the month — the way this rally has been going, that feels like a comically significant development. Exhaustion signs are aplenty but still not much to suggest the rally is breaking down just yet…

Returning to the 2 equity indices I’ve been closely watching:

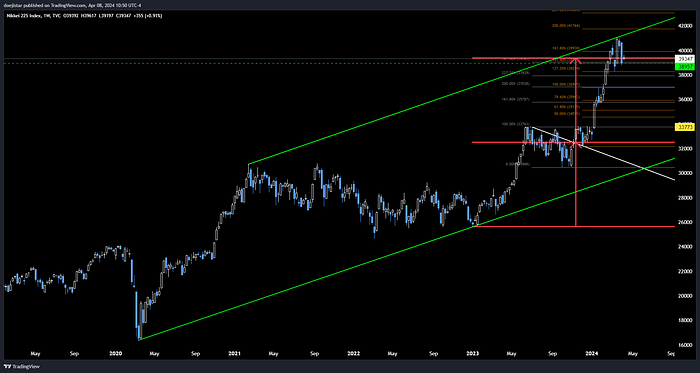

Nikkei has put in a full-bodied bearish bar last week to reverse all of the March gains. I am still short the index and still looking to see a meaningful close below this 39–40k region.

Swedish OMX is showing more tenative signs of exhaustion than the Nikkei is doing. It is reacting nicely to this technical zone and is yearning for a 3rd bearish weekly candle this week to get the correction going for European equities.

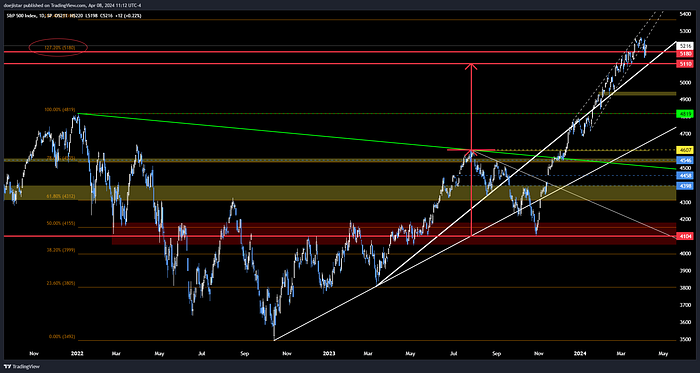

SPX has broken down from its rising wedge but the price action remains stubbornly resilient. I’m still holding out for a retest of the 5100 handle and some continued closes in this 5100s to print consecutive bearish candles. 10year nominal and real rates are continuing to push highs after the strong mtd-rebound and should continue to pose questions for risk equities.

NYFANG+ refuses to give up after sitting heavy on the 21ema last week. It’s attempting another push higher today as I write this during the NY morning session. No idea what to make of this chart but there is a well carved out trendline here that could cap rallies…

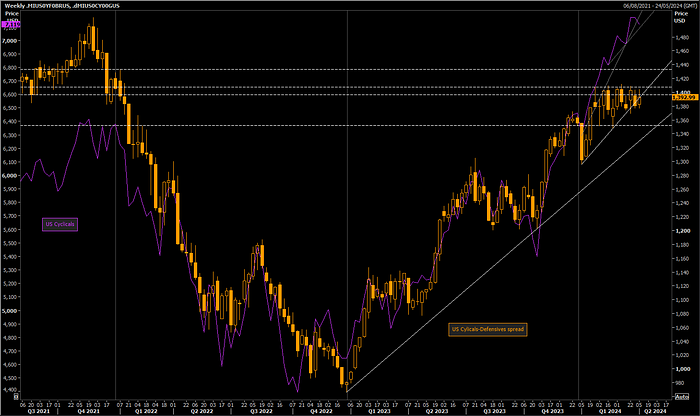

US Cyclicals remain stubborn but as flagged for many weaks, there are signs this theme is running on fumes. The prospects of fed cuts that have boosted this rally is becoming increasingly questionable as those prospects have diminished from 6 cuts to almost just 2 this year. Could the CPI this week give this chart some real signals of weakness?

Small/Mid-caps (yes, still) look structurally toppish. Not much else to say til it, either, shows a strong buying impulse higher, or rolls over from these levels I’ve been focused on for some time. Yields will guide my view here (as with US equities in general) given SMid’s sensitivity to rates.

Most-shorted stocks index as a fairly good sentiment indicator is showing cracks for the so-called ‘broadening rally’. I don’t think there is a chartist in the world that could be bullish on this chart, let’s put it that way.

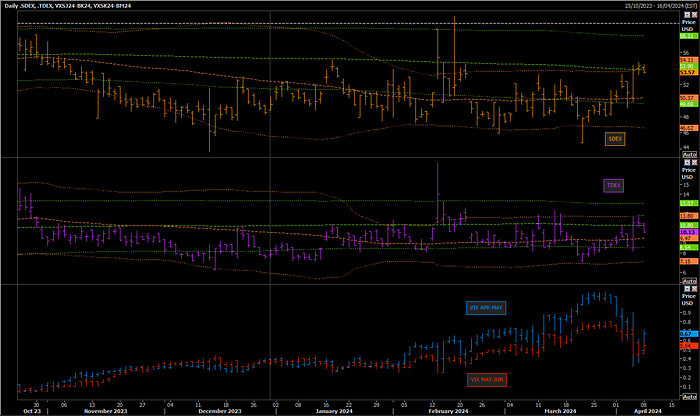

Volatility instruments are showing some increased uncertainty — Skew and Taildex are at slightly more elevated levels above 3month averages and while VIX has rolled off in recent sessions, it is pointing mildly higher.

COMMODITIES

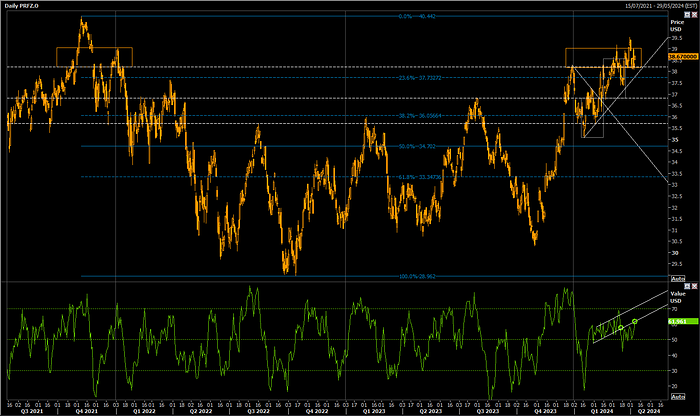

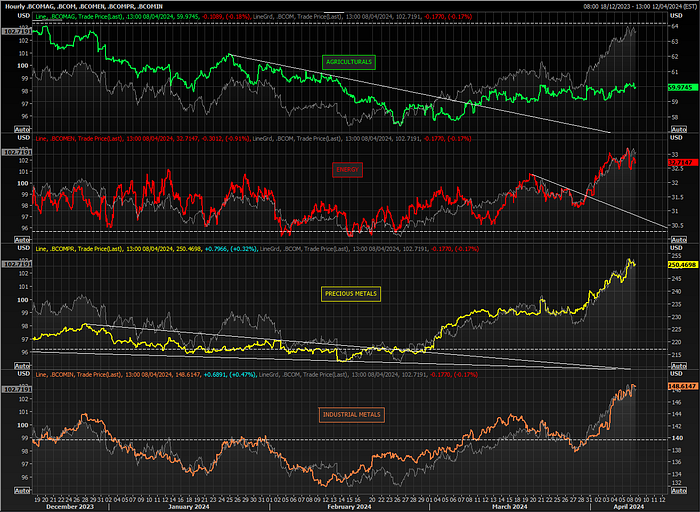

The commodities space is ramping, BBG index has put in the biggest weekly advance so far this year and since mid-June of last year.

Most of the rally owing to Precious and Industrial metals. Precious meals has some ridiculously strong momentum behind it, while Industrials are rallying on some improved China data. Energy is in consolidation at elevated levels while Agriculturals index in grinding away quietly.

WTI crude price action is suggesting that it will consolidate here and I’m interested in getting long in the low-80s.

HH Natgas is getting my interest again with price action looking more constructive thatn it did at previous lows. Its on course to printing a bullish engulfing today and would be technically constructive above the Dec and Feb lows.

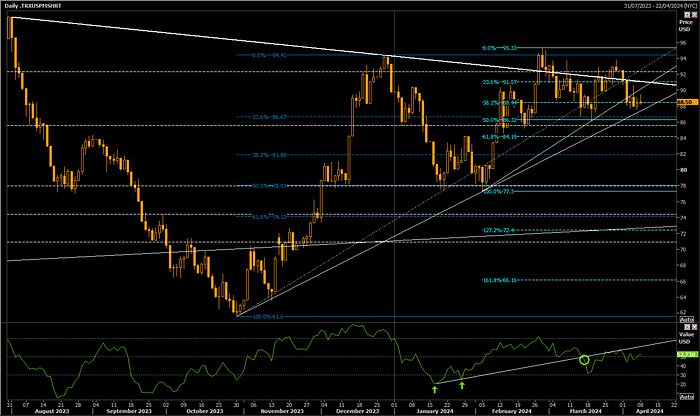

Gold / Silver was a short/long theme I wanted to trade dyanamically as I’ve noted about a month ago. I had some initial success with it last month but more recently, was too fixated on fading the Gold rally on the basis of rebound in yields that costed me missed opportunities in long Silver ideas. I think the spread is halfway through its journey lower and could consider it pre-CPI as it could be vulnerable to flushing out fresh longs. Silver is a touch chase up here but it would perk up my interest should it return to 26 or below.

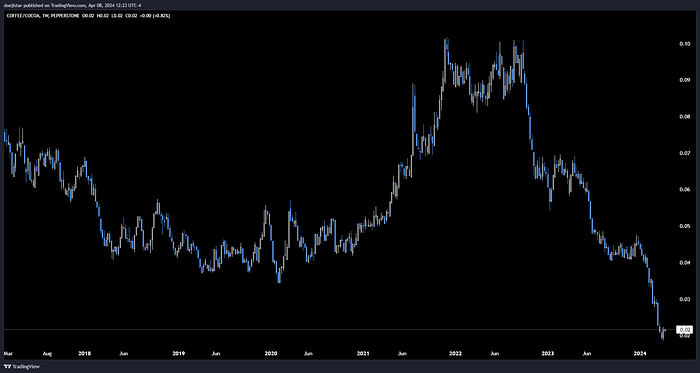

Coffee / Cocoa is a very attractive trade idea at the moment, a favourite of mate David Belle. I don’t see how you could put up the margin to trade this via futures, but if you trade CFD’s, it might be worth a look after the ratio printed a weekly bullish engulfing and newsflow in Coffee pointing to shortages beginning to be felt.

RATES

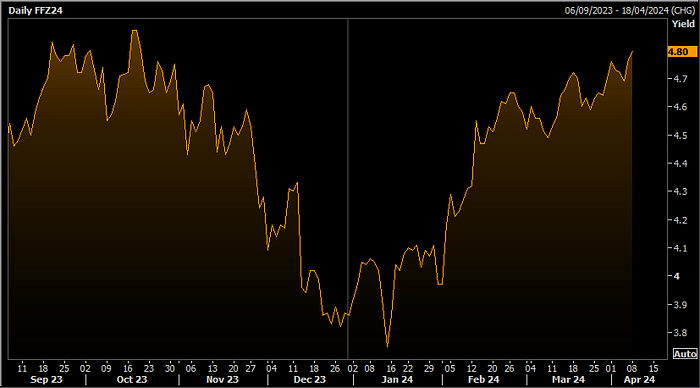

The main narrative in rates has been all about rate cuts being priced out.

The December fed fund futures made new lows to an implied rate of 4.8%, which is 53bps from the current 5.33% effective fed funds rate thus implying a market pricing for 2 cuts this year with US data continuing to show strength.

Rebound in economic data surprises (Orange) coincides with the rebound in yields 10yr yield (Purple) as well the December implied yield chart above.

10yr (top) has pushed strongly higher from the 4.2% level where I expected it to base out. It’s now pushing on beyond 4.4% and should it continue above 4.5%, I expect headwinds to equities to strengthen as well as boost USD.

10yr TIP yield is holding above 2%, a level above which equities (ES futures in Green) have particularly disliked — as marked by the vertical lines. Conversely when it has faded lower from the 2% handle, Equities are notably reassured and rallies again.

CURRENCIES

I maintain roughly the same view as I did in last week’s note for currencies and nothing much to add as I’m not keen in chasing the AUD rally at this stage nor buy into the EUR and GBP bounce for example. Key themes are to stay long USD against short EUR CHF JPY while interested in picking up CAD on dips on the crosses such as EURCAD NZDCAD.

That’s all for now. Good luck trading!