2024.03.11 Weekly

After getting hosed on good number of trades last week, I’ve decided to go flat into the weekend on the macro book and look forward with a clean slate. While a blip could be seen to be inevitable after a good long run, it leaves me reflecting on what I could have done differently as well as reevaluating my views.

Reflections …

Much of that poor performance came from holding onto a short JPY bias for too long on the expectation that the BoJ wouldn’t be signalling very much just yet, as well as bond yields to see a rebound and support the USD after coming off some 20–30bps from the Feb-highs. That view also had me attempting to fade Gold which put in a monster rally last week.

Some of that poor performance also came from expecting the risk rally to begin topping out while looking for some macro triggers to confirm it. It’s powered on higher and last week’s NFP didn’t offer any confidence that the risk rally would crater. In fact, it’s made me trade the upside in some stocks to hold into the Monday session. Beyond that, I still remain focused on two themes: 1) Rebound in bond yields, and 2) Pullback in stocks.

Where to for bond yields?

Since rates are essentially the underlying price of currencies of which assets are denominated in and valued, this is quite pivotal to my tactically bearish view.

Bonds saw quite the rally over the past few weeks and technically, they (via the FTSE World Government Bond index in Orange, and US10yr yield inverted in Purple) have made the natural retracement to the 38.2–50.0 area.

I have been theorising that the rally has been about short-covering, that is, shorts built up from the period of stronger than expected economic data (G10 Economic Surprise index inverted in Purple). As data surprises swung to the upside coming into the new year, Bonds sold-off, then rallied as the momentum in data surprises was lost in recent weeks.

Meanwhile Inflation (via the G10 Inflation Surprise Index) data has proved sticky. The turn lower in economic data surprises and higher inflation surprises while Central banks are resisting against cutting rates too soon, leads me to conclude that bonds rallied on stagflation risks ticking higher, or something to that effect.

The turn in economic surprises seems to be from the PMIs coming in shy of market expectations. But Global business activity as suggested by the S&P Global Composite PMI is signalling accelerating growth going up to 52.1 from 51.8 in January, to print 4 consecutive rising prints from the recent low point of 50.0 in October.

“Stronger demand conditions supported the latest acceleration in growth, with a steady upturn in demand for services accompanied by the first rise in new orders for goods in 20 months.”

Price pressures remain however — Higher prices for goods and services exhibits the strongest sentiment by managers across the sub-components, rising at a faster rate in February which has been “supported by the upturn in demand” with New Orders seeing the first rise for goods in 20 months.

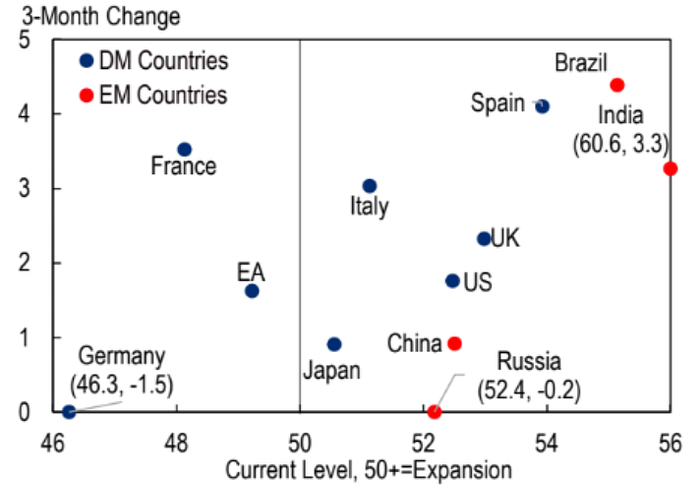

And the 3-month change shows a broad based rebound, but for Germany.

US10yr yields followed the 2 week decline in US data surprises, though last week’s NFP did provide an uptick in the surprise index. But 10yr yield was mostly unchanged after a flash move higher on the release which is the reason I noted NFP failing to provide any confidence that risk would be topping out just yet.

Bonds are beginning to look a little short-term overbought and looking ahead this week, we could see triggers for yields to rebound via Inflation and Retail sales data, and $90bln in bond supply.

Is risk pulling back?

Barclays had a good synopsis on the state of markets right now and sees it being in “reflation mode”. There is a sense that markets have raced ahead and its up to whether incoming data confirms a soft-landing.

Looking at the US and European Cyclical-Defensive spread, we are at an interesting point as I pointed out last week. It’s back to the support area of the 2021 highs which was the peak of the mega-stimulus induced reflation period. I think it extremely difficult to argue that we are in a cyclically stronger position now than we were then.

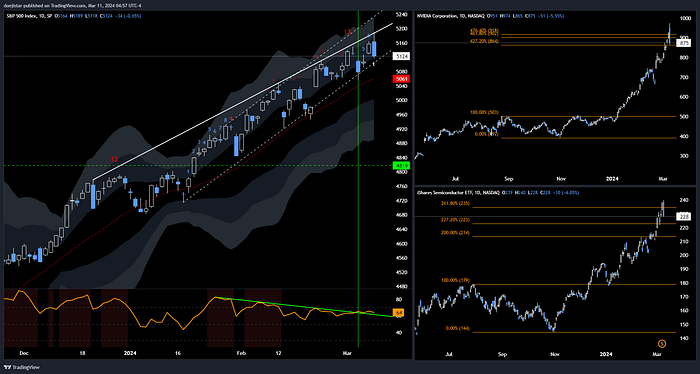

Looking at US stocks SPX and market leaders NVDA and SMH semi-conductors, we’ve printed a bearish engulfing on Friday. While backtests of the bearish engulfing signal alone isn’t particularly strong, it does tend to signal local tops when it comes after a long rally.

Snapshot from marketwatch.com shows it’s certainly got the markets attention and what that could mean for the broader rally.

NYFANG+ has been teasing bulls and bears alike last week but structurally, it is looking increasingly toppish. Momentum has completely fizzled out and threatening to swing towards a bearish bias (below 50).

Small/mid-caps liked the strong job gains reported but showing some tentative signs of stalling out. It’s probably one key segment to keep a close eye on this week.

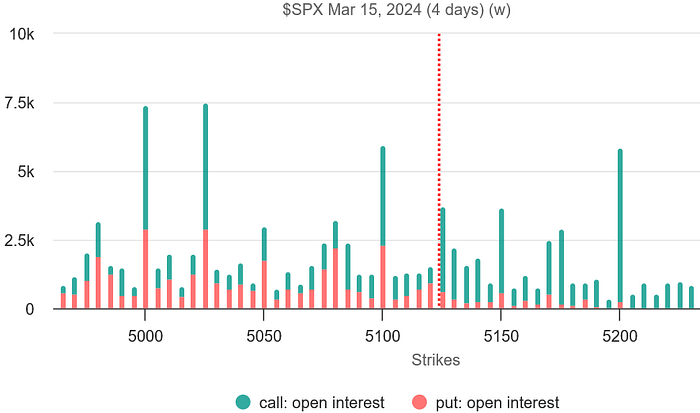

It’s OPEX this week and SPX options open interest is in an interesting spot. Early week downward momentum could accelerate as we sink towards 5100 and below but could see some sharp squeezes all the same, like we tend to see in the last couple hours of a trading day.

Overall, US equity charts have been in the process of ‘setting up’ a top over recent weeks and nearing technical confirmation. Considering what’s on the calendar this week and FOMC the week after, perhaps the market will lean on the prudent side?

NEWSFLOW

MARKETS

- Wall Street rallies, S&P 500 posts record closing high (RTS). It Isn’t Just Big Tech Propelling Gains in the Stock Market Anymore — A broader group of companies has fueled the recent climb to records (WSJ). US bond funds attract biggest weekly inflow since mid-2021 on rate cut hopes (RTS). Tech stocks see biggest weekly outflow on record — BofA (RTS). US job market data bolsters Fed’s ‘no rush’ rate cut view (RTS), Emergency Fed bank effort ends lending, as eyes turn to discount window (RTS). Bitcoin hits fresh record high above $71,000 as UK opens the door to crypto exchange-traded products (CNBC).

- Fed’s Powell: ‘not far’ from having confidence to cut interest rates (FT), Don’t expect a soft landing victory lap (RTS), ‘Worst case’ inflation fears threaten bond market calm (RTS), Fed likely to make ‘material’ changes to controversial bank capital proposals (FT). Williams: Neutral rate is likely still low (RTS). Mester: sees rate cuts later this year (RTS). Bowman: “Not yet” ready for rate cuts, willing to hike again if needed (RTS). Daly: Fed ‘focused and resolute’ on beating inflation (RTS). Kashkari sees two rate cuts at most this year (RTS).

- Central bankers see victory within reach in push to tame inflation — New data gives policymakers confidence they can cut rates by the summer (FT). BOJ’s growing confidence in prices, wages shifts focus to March meeting (RTS). Bank of Japan leaning toward exiting negative rates in March, sources say (RTS). Bank of Canada to hold rates steady as inflation eases and economy skirts recession (RTS). ECB keeps rates on hold but acknowledges some inflation cooling (RTS). Christine Lagarde signals June rate cut as ECB lowers inflation forecast — ECB president wants ‘more evidence’ to be sure inflation has been tamed and says it will have ‘a lot more’ data in 3 months (FT).

AMERICAS

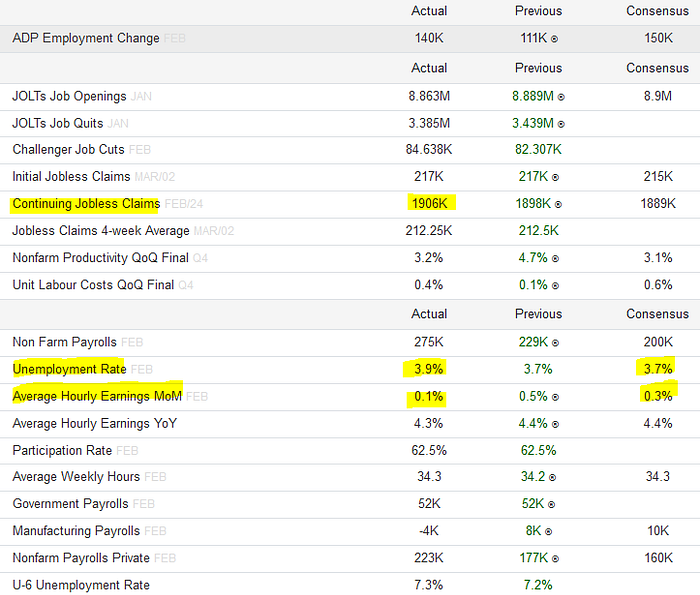

- Feb US payrolls show labor market healthy but not overly tight (RTS). US labor market cooling; unemployment rate rises to two-year high of 3.9% (RTS). US job openings fall marginally in January (RTS). Weekly jobless claims unchanged; trade deficit widens in January (RTS).

- US services sector slows in February; inflation moderating (RTS). US small businesses struggle for credit, one year after regional turmoil (RTS). US homebuying sentiment up; owners sense a ‘good time to sell’ (RTS). Yellen says Biden’s proposed housing tax credits could boost supply (RTS).

- Joe Biden to propose big tax rises for billionaires and corporate America (FT). Biden’s economic rating with voters flatlines despite improving outlook (FT). McConnell broke with Trump over Jan. 6. Now he’s endorsing Trump (Politico). Trump may have defamed E. Jean Carroll again, one day after posting a $91.6 million bond for last case (CNBC).

- Canada adds jobs in February as wage growth slows for second month in a row (RTS). Canadian services PMI rises to 4-month high in February (RTS).

EUROPE

- UK wage expectations fell below 5% in February (FT). UK house building activity declines at slower rate in Feb — Construction PMI recovered to 49.7, its highest level since August and up from January’s 48.8, but marking a sixth month below the 50 (RTS). UK firms report growth at 9-month high but price pressures mount, PMI survey shows (RTS). UK retail sales rose at slowest pace since 2022 in February — BRC says consumer demand was hit by bad weather (FT). UK Budget: Hunt and Sunak bet on tax cuts to revive UK election chances (RTS).

- Euro zone business activity moves closer to recovery, PMI survey shows (RTS). German institutes cut 2024 economic growth forecasts — IFO reduced its forecast to 0.2% from its previous projection of 0.7% in January citing weak consumption and high interest rates, IFW Kiel Institute lowered its forecast to 0.1% from 0.9% previously (RTS). German industry grows in Jan but car output remains weak (RTS). Recovery of the German economy remains a test of patience — DIW (RTS). Europe faces ‘competitiveness crisis’ as US widens productivity gap (FT).

ASIA

- Japan Q4 GDP revised up to slight expansion, economy avoids recession (RTS). Japan’s service activity grows in Feb on firm tourism (RTS). Japan household spending logs biggest drop in 35 months in January (RTS). Inflation in Japan’s capital re-accelerates in February (RTS).

- China’s services activity growth momentum softens in Feb, Caixin PMI shows (RTS). China’s exports top forecasts as global demand returns (RTS). Chinese trade rebounds on electronics and exports to Russia (FT). China’s consumer prices swing up on seasonal Lunar New Year gains (RTS).

- Australia economy slows to a crawl, underscoring case for rate cuts (RTS). Australia to Abolish Nearly 500 So-Called Nuisance Tariffs — Removing the tariffs will cost the budget $19.9 million in lost revenue annually (WSJ).

EQUITIES

Global equities looking a lot like the cyclicals-defensive spread noted above and again, it begs to question whether global equities can return to the stimulus-charged highs. Reiterating the previous week’s observation — this 127.2–161.8 fib region is usually a good area to look for a downleg and we’ve printed a full-bodied bearish bar on Friday. I look for another continuation bar within the first two days of the week to compliment that observation.

Further to the US equities charts earlier, the most-shorted stocks index is failing to maintain the break higher with Friday’s bar tailing down from above to close below the trendline.

I noted last week that there are hints of volatility creeping higher with the VIX front month contracts and a floor appearing in put premiums.

COMMODITIES

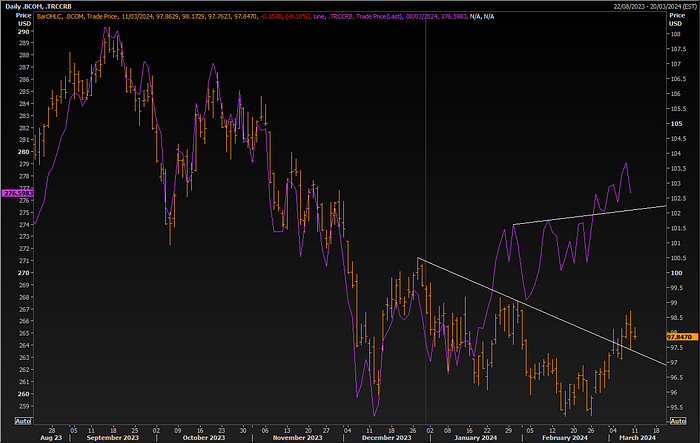

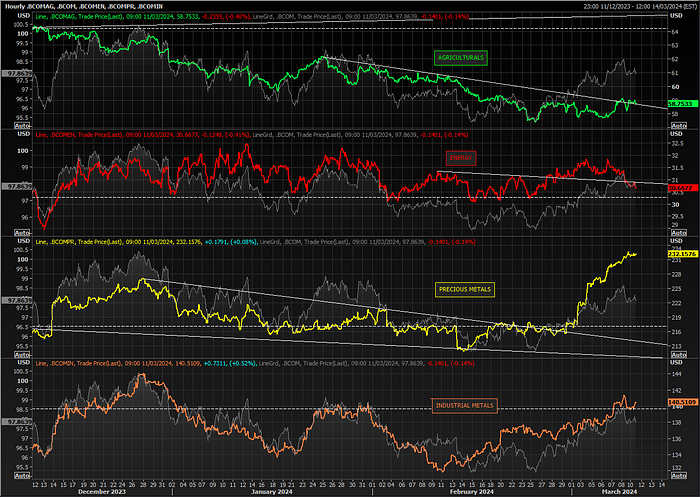

Bloomberg and TR-CRB commodities is holding a positive bias.

The big story has been in precious metals making a huge break higher, while Energy pulled back last week — the latter of which I’m positive about as noted last week and think pullbacks are good long opportunities for the longer term, particularly in NG.

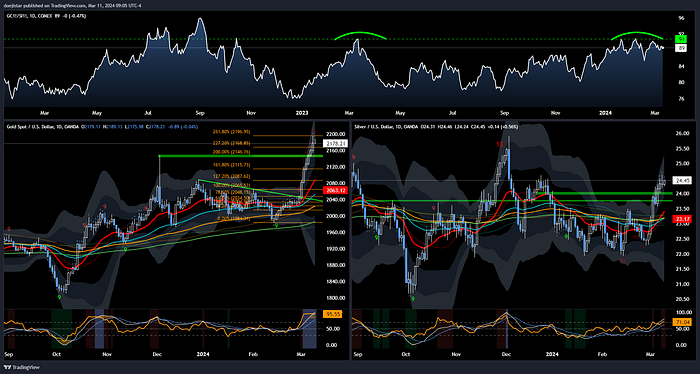

Taking a closer look at Gold and Silver for this week — the ratio has been rolling off from this key level which makes me particularly interested in trading this spread dynamically. Gold upside is looking extremely stretched while Silver looks like it could power higher to at least the 25–26 handles. This week I look to short Gold to the 2125/50 area to start and observe the price action thereon for a continuation lower, while long Silver on dips is on the radar with an eye on the 24.00 and 23.75 handles.

RATES

Yields continued to sag lower last week perhaps in response to the softer/loosening labour market data:

Slight miss on ADP though NFP beat, UE rate higher while wage growth softened, and Continuing claims continues its upward creep. ISM services employment came in a 48 vs 50.5 the month prior, and 45.9 vs the prior 49.1 for manufacturing.

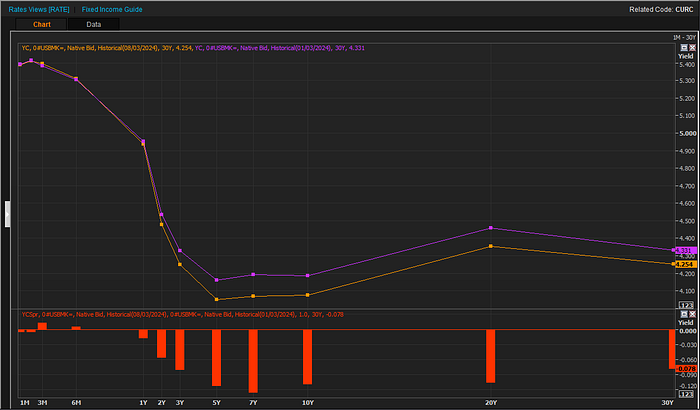

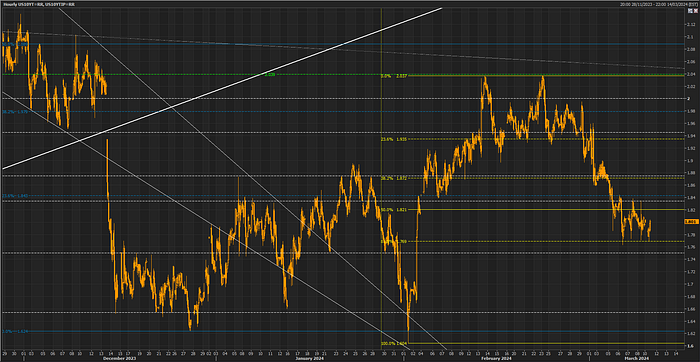

Looking at the 10yr yield chart however, the consolidation below the 50fib 4.85% mark is looking ‘bottomish’ and if it makes a recovery above 4.085% and 4.1% levels, I’d be positive about this being the ensuing range lows.

Interestingly, the 10yr TIP has bounced multiple times off the 61.8fib around the 1.77% mark, and should we have some strong data coupled with a moderate CPI print this week, this could well be the lows also.

CURRENCIES

In order of the strongest to weakest last week:

- JPY +1.12% put in a strong upward break in trend that is tough to ignore. I’ve paid the price dearly for holding onto a short bias even though I was becoming more skeptical, noting last week that I was “more cautiously bearish” on JPY. Sentiment for a BoJ pivot is gaining traction ahead of the meeting next Tuesday (Mar-19th) and regardless of whether I doubt they move just yet, the momentum trade is to chase cross-Yen lower (bullish JPY) up until the meeting.

- GBP +0.53% has hit major resistance and I think the trade is now to the downside. Manufacturing slowdown has decelerated, services remain resilient, but most of all — wage pressures appear to be easing, which would help to bolster the case for rate cuts. We get some employment data on Tuesday, and should it confirm a loosening labour market, I see Cable taking a peek below the 1.27 handle.

- AUD +0.42% strength has been a little surprising given weakening fundamentals and underwhelming announcements from China’s NPC. If it is riding on the broad risk rally, it’s looking like a good short at these levels after a strong reversal bar printed on Friday and index charts looking primed for a breakdown.

- NZD -0.02% similar technical picture to the AUD though for me, less preferred over AUD shorts. Nevertheless GDT auctions have been getting weaker of late and I like Kiwi lower as well.

- EUR -0.28% I’ve been bullish EUR via the crosses as inflation expectations ticked higher. I think that trade is now done as inflation expectations has come back down again while the EUR index has failed from both the 61.8 and 50fib last week.

- CHF -0.57% continues to drip lower and I see no reason for it to rebound meaningfully — maintaining a bearish bias.

- CAD -0.69% the BoC reiterated every meeting will be live as they look for a ‘high-degree of consistency’ that underlying price pressures are on the right downward track. While the overall tone from the BoC is leaning increasingly dovish, there is absolutely nothing new. Instead, I think the CAD has suffered from the crosswinds of the USD beating and based on the price action negative risk view, I expect it a slow drift towards the 200wma on the index chart above.

- USD -1.31% traded back down to a big support level and based on the views expressed throughout this note — potential for risk-off and yields rebounding, I think strength could reemerge and will be focused on USD longs across the board.

That’s all for now. Good luck trading!