2024.01.15 Weekly

My favourite board-game (aside Chess, if that counts) is Risk — a strategy game that requires a good ability of evaluating risks in both attack and defense. A failed attack, or even a successful one, comes with the risks of troop losses and weakening your overall army, whereas under-defended territories risks losing territory just as over-defended territories risk being under-deployed elsewhere leaving yourself with weak positions and less than optimal attacking chances. A good player is therefore able to carefully assess risk on every turn as he/she attempts to find the optimal strategy that is highly dynamic and dependent on the action of other players.

In the same spirit of the board-game, I’ve been attempting to find the optimal reward for my risk views since as early as late November after seeing one of the largest and steepest declines in financial conditions on record, aggressive pricing of rate cuts, and a monster rebound in stocks. Those developments led me to adjudge risks to skew increasingly to the downside the more that went on and that risk assets would face a reckoning or a reality-check of sorts.

This is how I feel we are set up coming into the new year:

“Investors were in a rather bullish mood last year. The buzz over generative AI and high expectations for company earnings helped stock prices soar. The belief in a “soft landing” scenario for the global economy, where inflation falls without triggering a significant slowdown, entered the mainstream. Traders also started to price in more interest rate cuts than central bankers were signalling, which meant that even bonds made a comeback. This year, all the optimism will be put to the test.” (FT)

With the market seemingly priced for perfection —that, the Fed will be reducing policy rates alongside a rapid decline in inflation without negatively impacting growth, and that market can be optimistic that stocks can maintain robust earnings growth for the year ahead. What seems certain to me is that the bar for even further optimism is extremely high, while the bar for disappointment is now extremely low. In other words, I don’t think it will take very much for the market rally to unravel if not consolidate lower.

This reminds me of the popular “Turtling in Australia” strategy which is to claim the Australian continent, defend a singular chokepoint, and to safely amass troops while other players fight it out. Overplaying this strategy however comes when a player fails to properly evaluate the risk of other players becoming too strong (or certain players too weak) that may result in an untimely advance out of Australia that is easily overpowered, and ultimately loss of the game. In effect, that player would have been ‘overly optimistic’ about their chances by delaying their advance that should have otherwise served to counter-balance opposing risks when timed right. Metaphorically, I see the market being that player — that is, the market has become overly optimistic to the point that it is in danger of becoming overpowered by opposing forces.

Some potential opposing forces that could impact markets:

- US shutdown risk — White House has told agencies to prepare for a shutdown with “some agencies to shutter on January 20 without new funding” according a recent BBG piece. Latest Sunday reports suggest congressional leaders have agreed on stopgap funding bill however which would keep the government funded til March. Should there be resolution this week, we could see some volatility as it draws scrutiny from rating agencies.

- Fresh upside risks to global goods disinflation brewing on intensifying geopolitical tensions. Given rates still at high levels, elevated debt and underlying inflation pressures lingering, Economies are likely to be in a weaker position to weather another wave of inflation than they were 2-years ago with little to no room for further policy easing.

- Aggressive rate cut expectations also at risk from reaccelerating inflation that could result in a sharp reversal in 2yr yields that has reached its lowest level since May last year.

- Tighter banking liquidity with BTFP expiring on March 11th which the banks have exploited since the regional bank crisis to profit from the risk-free arbitrage. The end of the program could result in selling pressure on these assets and volatility in Treasuries.

- RRP drainage while reserves are running scarce as a result of the Fed’s QT while long UST positioning (funded by via Repo) is crowded and disruptions in short-term funding markets could cause a significant deleveraging and volatility in bonds.

NEWSFLOW

MARKETS

- S&P 500 Falls Short of Record Despite Weekly Gain — The benchmark index is in striking distance of its record high (WSJ). European markets closed higher Friday, rounding off a largely negative week (CNBC). Tokyo Stocks Find Their Mojo as Bubble-Era Highs Draw Nearer — Some see all-time highs in view, signaling 10% rally this year, Valuations are far below dizzying heights of late 1980s (BBG). Price Wars Help Spark $157 Billion Rout in China Consumer Stocks (BBG). 2-year Treasury yield ends at lowest since May after producer prices data (MW). World Bank forecasts 2024 global growth to slow for third consecutive year — “Excluding the pandemic contraction of 2020, growth this year is set to be the weakest since the global financial crisis of 2009”. It forecasts 2025 global growth slightly higher at 2.7%, but this was marked down from a June forecast of 3.0% due to anticipated slowdowns among advanced economies. “Near-term growth will remain weak, leaving many developing countries — especially the poorest — stuck in a trap, with paralyzing levels of debt and tenuous access to food for nearly one out of every three people” (RTS).

- HSBC Says Goldilocks Scenario May Flip as Fed Cut Bets Overdone — Unwind may stoke ‘pain across the asset classes,’ recommends holding dollars, investment-grade bonds (BBG). More Stocks and Bonds Are Moving In Tandem, Worrying Some on Wall Street (BBG). Risk-On Markets Ignoring Inflation Red Flag — BofA Hartnett says geopolitical developments are inflationary (BBG). BofA Sees Tactical Sell in EM Currencies After US Inflation Data (BBG). VIX Trader Drops $17 Million on Bet That Eerie Stock Market Calm Won’t Last — “hard to know if it’s an outright bearish bet on the market, or an aggressive portfolio hedge after a big move. Either way, it expresses concerns that we could see a bit of a pullback during or after earnings season” (BBG).

- The Fed Launched a Bank Rescue Program Last Year. Now, Banks Are Gaming It — Borrowing at the bank term funding program is up to record highs but not because of new stresses (WSJ). Fed’s Barr Signals Emergency Loan Program (BTFP) Won’t Be Extended — Vice chair says that he expects use to continue until March 11 (BBG). Use of Fed Funding Tool Hits Fresh Peak as Officials Signal End — Use rose to all-time high $147 billion in week through Jan. 10 (BBG).

- US inflation outstrips forecasts with rise to 3.4% for December (FT). Bond Market Adds to Fed Rate-Cut Bets Despite Inflation Uptick — Expectations mount for easing beginning in May (BBG). Traders boost bets on Fed rate cuts after producer prices slide (RTS). Atlanta Fed boss warns US progress on inflation is likely to slow — Raphael Bostic believes rates need to stay on hold until at least summer to prevent prices from rising again (FT). Too early to declare victory over inflation or recession, PIMCO says — “At this point, we don’t see duration extension as a compelling tactical trade, we expect to be broadly neutral on duration after the most recent bond-market rally, which has brought global yields back in line with our expected ranges, and amid the shifting balance of inflation and growth risks” (RTS). Global Inflation Was About to Be Tamed. Now Red Sea Attacks Fan Revival Fears (BBG). Fed officials say December CPI did not budge view of inflation — Goolsbee: data marked the final month of a “hall of fame” year for inflation reductions, and though housing inflation came in a bit hotter while services inflation improved more than anticipated; Mester: December CPI report “just shows there is more work to do and that work is going to take restrictive monetary policy, I think we need to see more evidence” before reducing interest rates, with a March rate cut, currently anticipated by financial markets “too early in my estimation”; Barkin: inflation report was “about as expected, this gap between services and shelter and goods is one that I am watching carefully because you would not want a goods deflationary cycle to end and find yourself disproportionately bearing the cost of shelter and services, you’d have even more reassurance…if it were broader based” and included a slower pace of price increases for services and housing costs (RTS). Markets tweak Fed balance sheet views after comments from Dallas Fed chief — Lorie Logan explained how contracting liquidity in money markets may sway the outlook for QT. “In my view, we should slow the pace of runoff as ON RRP balances approach a low level. Normalizing the balance sheet more slowly can actually help get to a more efficient balance sheet in the long run” by making it easier for financial firms to adjust their individual liquidity levels. Goldman Sachs economists said in a note “but in that case, runoff should last a bit longer and the terminal size of the balance sheet should end up in roughly the same place, so the macroeconomic effects of starting earlier should be very minor”. Evercore ISI said “Logan is not signaling an early end to QT” and it remains likely a tapering of QT will start in summer. BofA economists now project Fed officials will announce a tapering of the drawdown at the March FOMC meeting while holding onto the view QT will end in summer (RTS).

- White House Tells Agencies to Prep for Shutdown Amid House Chaos — House GOP split over spending deal Johnson cut with Schumer, Some agencies to shutter on January 20 without new funding (BBG). US Economy Set for Another Cash Boost If Congress Backs Tax Deal (BBG).

- Harley Bassman Says the Treasury-Yield Curve Is Set to Return to Normal — “It’s done. Stick a fork in it, man. The 10s aren’t moving. And I think the 30-year rate, it probably goes up from here as the curve resteepens again, All the action’s the front end, that’s where all the action’s going to be.” (BBG). Bond Sales Reach €108 Billion in a Record Week for Europe (BBG). Investors warn governments about high levels of public debt — ‘Out of control’ fiscal deficits set to resurface as a concern for markets (FT). Emerging market debt issuance hits record as borrowing costs fall — Developing country governments and companies issue $51bn of bonds in a rush to lock in lower yields (FT). Investors warn of ‘complacency’ over junk bond risks — Yields have fallen to about 8% from 9.4% in early November but some analysts are concerned by high funding costs (FT).

- Bitcoin Retreats From 2-Year High on First Day of ETF Trading — SEC approved ETFs after markets closed on Wednesday, over $4.6 billion has changed hands in early trading (BBG). SEC’s bitcoin ETF sign-off comes with a stark reminder of its lingering doubts (FT). MicroStrategy’s Saylor Sold Shares Daily in Runup to ETF Launch (BBG). Vanguard’s decision to shun bitcoin ETFs triggers backlash — with some customers moving to crypto-friendly competitors like Fidelity (MW).

- Yemen’s Houthis launch their largest Red Sea drone and missile attack, though no damage is reported — forcing US and British navies to shoot down the projectiles in a major naval engagement (AP). US, UK launch retaliatory strikes against Houthis in Yemen (TheHill). US Launches Fresh Yemen Strike a Day After Broader Attack (BBG). Oil’s Red Sea Pinch Point Could Get Tighter After US Airstrikes (BBG). Oil tops $80 a barrel after Houthi threat diverts tankers from Red Sea (FT). Oil Tanker Owners Abandon Southern Red Sea Trips After Yemen Airstrikes (BBG). Russia Reduces December Crude Output by Most Since Cuts Started (BBG). Surge in Freight Reverberates Through the Global Oil Market — Higher costs spur Asian buyers to favor Mideast crude over US (BBG). Maersk chief warns Red Sea shipping disruption may last for months — Vincent Clerc says container ship attacks by Houthis could have ‘significant consequences’ for global growth (FT). Shippers turn to air freight to alleviate Red Sea crisis — Mix of sea and air favoured to avert delays on Asia-Europe routes while limiting costs (FT). Reinsurers pull back from Israel and Middle East risks — Firms inserting get-out clauses into policies to protect against a full-scale regional conflict (FT).

- Moscow imports a third of battlefield tech from western companies — Ukrainian officials find US and European components in Russian equipment (FT). Missiles from Iran and North Korea boost Russia’s onslaught on Ukraine (FT).

- Battery Metal Price Plunge Is Closing Mines and Stalling Deals (BBG). Copper Declines as Traders Mull Rate Path After US, China Data (BBG).

- Tesla Gets a $94 Billion Reality Check as EV Winter Sets In — Valuation hit biggest ever for Tesla in first 9 days of a year, China price cuts, Hertz’s EV sale, plant shutdown sour mood (BBG). Tesla Declines on China Price Cuts and German Plant Shutdown (BBG). Tesla Stock Is Being Sold by Almost Everyone, Cathie Wood Is Buying (Barrons). BYD’s Biggest Bull Cuts Price Target by 23% on Dimmer Outlook — Citigroup lowers sales forecast for 2024 to 3.68 million units, Target cut on slowdown in China, intensified competition (BBG).

AMERICAS

- Rising shelter, healthcare costs lift US consumer inflation in December — Consumer price index rises 0.3% in December, Shelter accounts for more than half of rise in CPI, Core CPI gains 0.3%, Weekly jobless claims fall 1,000 to 202,000 (RTS). US consumers see smaller inflation gains ahead, New York Fed says — consumers’ projection of inflation over the short run fell to the lowest level in nearly three years in December (RTS). US producer prices unexpectedly fall; goods deflation seen persisting — Producer price index falls -0.1% in December vs +0.1% Goods prices dropped 0.4%, with a 12.4% decline in the cost of diesel fuel accounting for half of the decrease; Core PPI increases 0.2%. “The key upside risk to inflation is from the war in the Middle East and potential disruptions to trade flows and global energy supplies,” said Bill Adams, chief economist at Comerica Bank in Dallas. “But petroleum and renewables output are growing faster than GDP in the U.S., which so far has offset the impact of geopolitical risk and kept energy prices well behaved” (RTS). US small business sentiment up, but labor, inflation worries persist — NFIB index rose to 91.9 in December from November’s 90.6 for the first time in five months, but hiring costs and ongoing concerns around inflation continue to sour business owners’ confidence (RTS).

- US Home-Purchase Applications Increase in First Week of 2024 (BBG). US homebuyer confidence up in December, more see loan rates falling — Fannie Mae Purchase Sentiment Index rose 2.9 points to 67.2 in December, up 6.2 points year-over-year. “Notably, homeowners and higher-income groups reported greater rate optimism than renters; in fact, for the first time in our National Housing Survey’s history, more homeowners, on net, believe mortgage rates will go down than go up”. “Homeowners have told us repeatedly of late that high mortgage rates are the top reason why it’s both a bad time to buy and sell a home, and so a more positive mortgage rate outlook may incent some to list their homes for sale, helping increase the supply of existing homes in the new year. Like many others, even if rates fall further, we continue to believe that affordability will be tempered in part by elevated home prices, especially for first-time homebuyers, and we expect the pace of home sales improvement to be modest in 2024” (RTS). Bad Office Loans Mount at Bank of America, Wells Fargo — Big US banks reported more charge-offs for struggling debt, US office values have fallen on higher vacancies and rates (BBG).

- $6 Trillion in Taxes Are at Stake in This Year’s Elections — Biden, Republicans offer vastly different plans for handling tax cuts that lapse after 202 (WSJ). Gold-standard Iowa poll shows Trump is cruising — Nearly half of likely caucusgoers said they would vote for Trump (Politico). Trump doesn’t just lead — he’s dominating the race in nearly every way — 5 takeaways from the big new Iowa poll — Trump voters have all the energy; Haley could be weaker than the numbers suggest; DeSantis may have a turnout advantage; Where Trump’s hold over the GOP is strongest; The evangelical vote favors Trump (Politico). The Vivek Ramaswamy Show Approaches its Finale — The 38-year-old entrepreneur’s campaign has been filled with outrages and provocations. Are the Iowa caucuses his last stand? (Politico).

- Toronto’s Downtown Office Vacancy Hits Record With More Supply (BBG).

- Mexico’s headline inflation up in December, core rate down — “reflected a spike in agricultural prices, with fruit and vegetables inflation hitting a two-year high” (RTS).

EUROPE

- ECB rate cuts not a near-term topic, Lane says — Recent inflation data broadly confirmed current thinking at the European Central Bank, meaning interest rate cuts are not a near-term topic of debate (RTS). Eurozone heading for another downturn, warns ECB vice-president — Rapid pace of disinflation seen last year likely to ‘slow down’ in 2024 (FT). UK could beat US and euro zone to sub-2% inflation — Capital Economics — “These drags aren’t as powerful elsewhere,” Paul Dales, chief UK economist at Capital, said in a note to clients. “If we’re right, then in April, inflation in the UK will be lower than in the US and the euro-zone for the first time in two years” (RTS). BofA expects BoE to keep its bank rate on hold until August 2024 — expects rate cuts of 25 basis points per quarter from there, “BoE will be the last of the major central banks to start the cutting cycle and it is likely to move slower, at least compared with the ECB” (RTS).

- UK economy at risk of recession despite November growth — UK GDP +0.3% m/m in November vs +0.2% poll forecast, GDP shrinks 0.2% in 3 months to November, UK at risk of recession without growth in December, Inflation and higher interest rates weighed in 2023, Economists see less pressure on households in 2024 (RTS). Hopes for lower inflation add to signs of life for UK economy — Analysts say price growth will slow more quickly than Bank of England predicted if Middle East tensions do not escalate (FT). Tories facing 1997-style general election wipeout — YouGov survey, most detailed in five years, predicts that Conservatives will retain just 169 seats as Labour sweeps to power with 385 (Telegraph).

- Eurozone unemployment returns to record low of 6.4% — Continued rapid wage growth will add to ECB worries about the timing of a potential interest rate cut this year (FT). German wholesalers sound alarm as sentiment ‘on the floor — German wholesalers expect revenues to fall 2% in nominal terms this year, continuing a downward trajectory after a 3.75% decline last year; In real terms, association of wholesalers and exporters expects a 1% decline for this year following a 4.25% contraction in 2023 (RTS). German industrial output drops unexpectedly in November — The decline in output was broad-based. The production of capital goods decreased by 0.7% on the month, the production of intermediate goods fell by 0.5% and that of consumer goods by 0.1%. Outside manufacturing, there was a 3.9% increase in energy production, while production in construction dropped by 2.9% from the previous month. “companies are increasingly reacting to falling order books"; “German industry was still in recession last quarter”; “With a soft or hard landing of the U.S. economy and still very little positive growth momentum in China, external demand for German industrial production is likely to remain weak” (RTS). German insolvencies set to rise as Covid aid ends and economy stagnates — Well-known companies including Galeria Karstadt Kaufhof and Bree have filed for insolvency this year (FT).

ASIA

- Taiwan Elects US-Friendly President, Defying China Warnings (BBG). US delegation heads to Taiwan after voters defy China — Two former officials sent by President Joe Biden will arrive in island state later on Sunday (FT). Taiwan Election Result to Force Compromise in Boost for Markets — Ruling DPP won presidency but lost legislative majority, Analysts say ‘status quo’ outcome should bode well for markets (BBG).

- China’s exports rise, but deflation persists as economy enters 2024 on shaky footing — Exports growth picks up pace, signals turn in global trade, Analysts say trade impulse not enough to boost domestic demand, Consumer and producer prices highlight stubborn deflationary pressure, More policy support seen as economy still fragile heading into 2024 (RTS). China’s Loan Growth Falls to Record Low as Demand Struggles — Financing and loan growth miss expectations in December (BBG). China Pledges to Boost Developer Lending to Tackle Home Sales Slump (BBG).

- BOJ seen sticking to forecast of inflation staying near target, sources say — BOJ seen cutting fiscal 2024 core inflation forecast, No major changes to BOJ’s ‘core core’ inflation forecasts, BOJ widely expected to keep ultra-easy settings in January (RTS). Japan’s Nov real wages down for 20th straight month — “It’s too early, if not misleading, to judge the winter bonus trends from November’s special payments figure alone,” a labour ministry official said. Japanese businesses are entering the collective pay talks season known as “shunto”, which culminates in March. Last year, major firms struck a deal with unions that resulted in the largest pay rises — 3.58% — in three decades amid four-decade-high inflation. (RTS)

- Australia inflation slows to 4.3% in Nov, core down sharply — CPI dropped to a near two-year low (RTS). New Zealand Home-Building Costs Rise at Slowest Pace Since 2016 (BBG).

- Turmoil at South Korean builder revives risk fear after Legoland credit crunch — builder’s distress recalls a liquidity crunch in 2022 triggered by the default of a Legoland theme park developer that pushed some corporate borrowing costs to the highest level in more than a decade (FT). South Korea Alleges Naked Short Selling by Two More Global Banks — Two banks breached rules while shorting 5 Korean stocks (BBG).

- India’s retail inflation rises to four-month high in December on higher food prices (RTS).

EQUITIES

ACWI global equities index is showing more signs of exhaustion — weekly MFI now overbought to add to the RSI overbought reading printed in the last week of 2023

EMXC Emerging markets ex-China is setting up for potential failure at the Dec14th high and a right shoulder with weakening momentum, and EFA Developed markets index is also showing the same signals. A close at last week’s low or lower would expose a move the 38.2fib at the least.

SPX is back to within less than 1% of ATHs but broader momentum is on a weakening trend — I continue to look for a pullback to the 4550–4600 area.

OEX large-caps index continues to lead US equities higher, but there are signs of caution being Weekly overbought and Daily momentum rolling over.

NYFANG+ made new ATH last week but finishes with some indecisive price action with RSI hinting potential weakness.

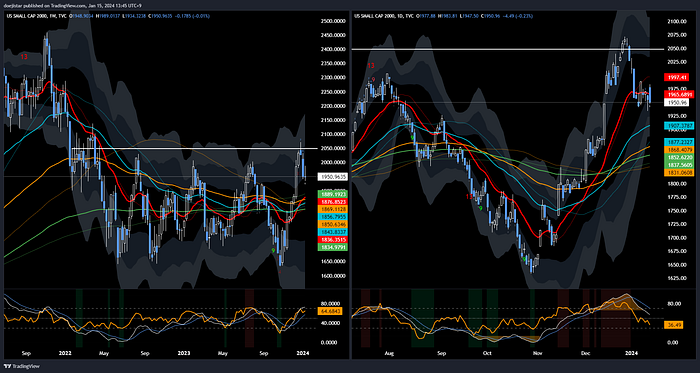

RUT small-caps is looking the weakest of the major indicies, with daily price action still sitting heavy with momentum in bearish territory.

Most-shorted stocks index, often a good measure of sentiment strength has put in a 3rd consecutive week of losses looks well on its way to the 38.2fib.

While VIX remains at extreme lows, there has been a slight pick up in hedging demand over the past month. With skew being very cheap as equities sit near ATH, and potential risks to inflation and policy expectations in the weeks and months ahead, I would be very surprised if put premiums doesn’t continue to pick up even at a slow pace.

Nikkei is getting a a great deal attention as it charges higher to push new 35-year highs. It is extremely overbought across all higher timeframes however where one would probably expect some consolidation at some point and I would expect the rally to consolidate at some point after a 10% rally off the Jan4th low.

DAX price action is looking very sluggish in comparison the indices above. Another daily close below the 20dema would suggest a pullback after making new ATH last month is in order, especially with economic data deteriorating.

European equity sentiment is notably weaker since the highs last month, while the US does not yet appear ready to concede on the soft-landing narrative. Interestingly the spread between US and European cyclical sectors is within touching distance of the 2021 high that marked the end of US monetary easing where it would seem fitting to see the spread turn from these levels should the narrative shift towards delayed cuts.

COMMODITIES

Bloomberg commodities index been more or less flat over the past month.

Agricultural commodities prices has sagged through Q4 and into the new year — which isn’t particularly ununusual given the seasonal pattern of fresh harvests around the end of the year. Energy prices are grinding higher and Precious metals holding key support amid on going geopol tensions. Industrial metals continues to trade heavy as global manufacturing remains in a slowdown.

While I have been trading in and out of WTI longs, I’m rethinking how I should be trading Crude last week. Firstly, I’ve noticed US sessions have tended to see some aggressive selling in Crude and Secondly, I’m starting believe that US crude is more shielded from the middle-eastern conflict given the strong rebound in production. The move in Brent-WTI spread reflects over the past few months reflects that, and I see the spread continuing to move in Brents favour while tensions persist. On trading them individually, I look to trade around buying Brent on dips, and tactically selling WTI on rips.

Precious metals Gold and Silver are both showing constructive price action and similar to Brent WTI trading theme, I will have long Gold and short Silver or rips theme in mind.

RATES

Increasingly dovish rate expectations has dragged the yield curve lower led by the front end. 2yr fell ~25bps the past week as the market projects (from what I’ve observed from twitter) a weakening December core-PCE from the CPI despite it beating expectations.

Market has been on a bull steepening regime for the last 6 months but I think there is a serious risk of this trend being disrupted as I’ve highlighted above. A potential reacceleration in inflation for the coming months could see a bear flattening in the yield curve, and BTFP expiring may see some unwinding in short-term money markets and short-end of the curve.

Front end of the yield curve has seen a big fall

US 2-year Treasury yields fell for six straight days, losing 23bp on the week.

US 5-year real rate

US 2s vs G7 2s

CURRENCIES

It’s somewhat surprising how resilient the USD has been so far this month given the big move in US 2yr yield and narrowing in 2yr spreads. Ordinarily one would have to take a short USD bias based on these moves but perhaps the diverging fundamentals helps to explain USD resilience which, would be help to provide USD longs some confidence that losses could stay limited while the trade awaits for potential risks to materialise.

Weekly and [Daily] G8 index observations, from strongest to weakest:

- GBP +0.44% strongest closing out at the 50fib of the Aug-Oct range where there is some decent resistance from here upwards [Some selling pressure seen the last 2 sessions given the long lower wicks]

- EUR +0.21% positive week but rally capped by the trendline and 20wema once again [well offered at resistance and trendline above]

- USD +0.12% unable to follow through from the rally seen on the first week of the year as aggressive Fed cut expectations remained in tact through CPI and PPI data [consolidating between strong resistance above while 20dema below holds —I’m marginally leaning towards a breakout than a breakdown]

- NZD +0.05% roughly unchanged for the past few weeks, holding up for now but momentum potentially rolling over [showing signs of upside exhaustion with a potential right shoulder]

- JPY -0.10% holding prior week’s low and around the pivot level of the September low and November high [broke below the pivot area which could now serve as resistance with the rebound coming from below]

- CHF -0.18% rally stalling to start the new year but broader picture remains strongly bullish [series of lower highs and lows — bullish consolidation or rolling over?]

- CAD -0.28% constructive technical picture continues to fade as it struggles to hold gains and trades heavily below the ema’s and trendline [Daily price action points a potential break lower]

- AUD -0.39% continued to rollover closing the week around key support but momentum increasingly negative [vulnerable as it trades heavily into the trendline]

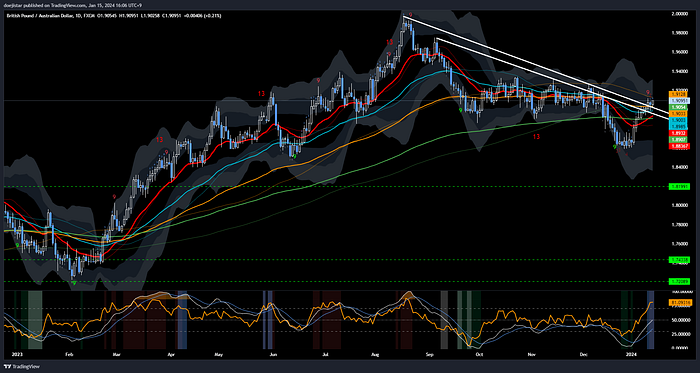

Last week I flagged a potential breakout in GBP crosses. GBPAUD has broken out and weekly momentum (strongest vs weakest) favours further continuation. There are some overbought signals on the chart, but when crosses like these begin to trend, those signals should largely be ignored.

As for the USD majors, I’ve been a little unsure about EURUSD and GBPUSD and went with USDJPY long around 143.70 last week which seems the cleanest way to express the upside risks to US yields. I have retained some longs into the weekend and will look to add on dips.

That’s all for now, good luck trading! //